AI Credit Repair Tools: An Honest Comparison

Dovly, ChatGPT + ScorePivot, and Credit Booster AI are growing fast. Here’s a clear-eyed look at what each one actually does — and what it won’t.

AI Credit Repair Tools

AI Credit Repair Tools

There is something quietly absurd about the credit repair industry’s online presence. Search for an honest comparison of any two AI credit tools and you’ll find one of three things: a glowing review written by the company itself, an affiliate article that earns a commission for every signup it generates, or a forum thread full of people asking the same question you just typed. What you almost never find is a straight answer.

AI credit repair tools are no longer fringe products. Dovly claims over 1.5 million users. ScorePivot is being pitched to thousands of entrepreneurs wanting to launch credit repair businesses. Credit Booster AI positions itself as a hybrid coaching platform. ChatGPT, meanwhile, has become an unlikely DIY credit repair tool for millions of people who realized they could paste their credit report into a chat window and ask it to write a dispute letter. The category is real, it is growing, and it is almost entirely unreviewed by the outlets that could actually help consumers make a good decision.

So let’s do that.

First, the Baseline Truth About Credit Repair

Before comparing any tool, there’s one thing every honest article has to say upfront: no AI — and no human, and no law firm — can remove accurate negative information from your credit report. Not one. If you missed three payments in 2022 and those payments are correctly recorded, they stay on your report for up to seven years, full stop. That’s federal law under the Fair Credit Reporting Act (FCRA). Any service that implies otherwise is either misleading you or hoping you won’t read the fine print.

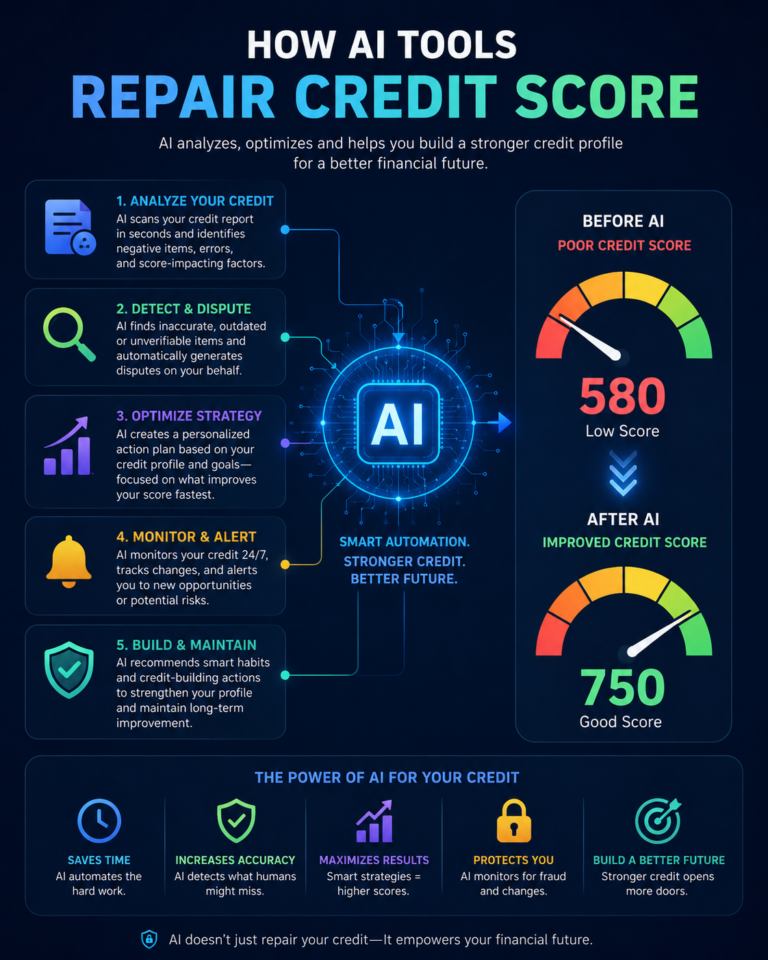

What AI tools can do is automate the process of finding inaccurate information — wrong balances, duplicate accounts, debts that aged off but weren’t removed, payments marked late that weren’t — and then help you dispute those errors with the credit bureaus. The FTC has estimated that roughly one in five Americans has an error on at least one of their credit reports. That’s a meaningful number. There is real work to be done here. The question is which tool does it best, at what price, and with what trade-offs.

Dovly: The Closest Thing to a Mainstream AI Credit Tool

Dovly is the most established AI-first credit repair product on the market. Founded in 2018 by Nirit Rubenstein and Tedis Baboumian in Phoenix, it has quietly grown into a platform with a genuine user base and verifiable results — which, in this space, already puts it ahead of most competitors.

How it works: After signing up (no hard credit pull), Dovly connects to your TransUnion report. Its AI scans the report for negative items — late payments, collections, hard inquiries, charge-offs, accounts that may have aged out — and flags them for dispute. Disputes are generated and submitted automatically on your behalf. Unlike a one-time letter-writing service, Dovly operates continuously, creating new dispute cycles each month across multiple items simultaneously. You monitor progress through a dashboard, and the company sends periodic updates as items are resolved.

Pricing: Dovly offers a free tier with meaningful functionality — monthly TransUnion score access and the ability to manually trigger disputes. The Premium plan costs $39.99 per month or $99.99 per year, which unlocks fully automated disputes, more dispute volume, credit builder tools, and fraud protection features. Compared to traditional credit repair services that often charge $100–$300 per month, this is substantially cheaper.

What the numbers say: Dovly reports that free members see an average score improvement of 38 points while Premium AI members see an average of 93 points, based on members enrolled for more than six months. Those are self-reported averages from Dovly’s own data, which matters — the sample isn’t independently audited. However, the numbers are consistent with what users report on Trustpilot and in app store reviews, where complaints are largely about billing and cancellation rather than about the product failing to work at all.

What it doesn’t do well: Dovly works almost exclusively through TransUnion. If your worst errors are on Equifax or Experian, you’re largely on your own. Some users who upgraded to Premium have also reported that the “AI” dispute process still requires more manual input than advertised — selecting accounts, choosing dispute types, and confirming reasons rather than having the platform do everything autonomously. One App Store review put it plainly: “The main thing that AI is supposed to do is handle and execute complex tasks within a short time. Dovly seems to have a simplified approach, but each of its features feels half baked.”

That criticism is worth sitting with. Dovly is genuinely useful and more affordable than alternatives, but describing it as a full-service autonomous AI engine is a stretch. It’s more accurate to call it a well-designed automation layer on top of a dispute process you still have to manage to some degree.

Best for: Budget-conscious users who primarily have TransUnion issues, want something set-and-forget, and are comfortable with a software-first product that has limited human support.

ChatGPT + ScorePivot: Two Very Different Uses of the Same Idea

This pairing requires a bit of unpacking because “ChatGPT for credit repair” and “ScorePivot” are not the same thing at all, even though they both involve AI.

ChatGPT as a DIY Credit Repair Tool

This is genuinely one of the more interesting developments in personal finance in the last few years. People have figured out that if you paste the text of your credit report into ChatGPT and give it the right prompt, it will identify potential errors, cite relevant FCRA provisions, and draft customized dispute letters tailored to specific accounts and specific bureaus.

The approach works — to an extent. Users have documented real-world results. One account on Medium described disputing errors using ChatGPT-generated letters with FCRA citations (specifically 15 U.S.C. § 1681i and § 1681s-2), getting two collections deleted and a late payment corrected within 30–45 days. A goodwill letter drafted with ChatGPT’s help got a lender to remove a single late payment as a one-time exception.

What’s notable about this approach is that it has no monthly fee, produces highly customized output rather than generic templates, and treats the user as someone capable of following through on a process rather than someone who needs to be managed. The trade-offs are significant, though. ChatGPT does not connect to your actual credit reports — you have to pull them yourself from AnnualCreditReport.com and paste relevant sections in. It has no tracking dashboard, no automated follow-ups, and no ongoing monitoring. If a bureau reinserts a removed item (which happens), ChatGPT won’t know unless you tell it. It is a tool, not a service.

Credit bureaus have also become more aggressive about flagging dispute letters that appear generic or mass-produced. ChatGPT’s advantage here is genuine — letters can be made specific and unique — but only if you prompt carefully and don’t just use the first output it gives you.

ScorePivot: A Platform for Running a Credit Repair Business

ScorePivot is often lumped into this conversation, but it’s doing something categorically different. It is not a consumer credit repair product. It is software designed for people who run credit repair businesses — tracking client files, automating dispute letter generation at scale, managing compliance workflows, and handling client communications. If you want to start a credit repair company, ScorePivot is a tool you’d evaluate. If you want to fix your own credit, it is not the right product.

That distinction matters because a lot of content conflates the two. ScorePivot is pitched with language about AI dispute automation and score improvement, but the audience is always the entrepreneur managing 50 clients, not the individual trying to remove a 2020 collection. Knowing this saves you from signing up for the wrong thing.

Best for ChatGPT DIY: People who are organized, willing to invest a few hours in the process, have straightforward errors to dispute, and want to avoid any ongoing subscription fees. It rewards effort.

Best for ScorePivot: People who want to operate a credit repair business and need client management, compliance tools, and scalable dispute automation.

Credit Booster AI: Coaching and Disputes Combined

Credit Booster AI is the newest entrant in this comparison and also the hardest to evaluate fairly, because almost all of the “reviews” that show up in search results are from the company’s own website. When a site publishes pieces titled “Credit Booster AI vs. [Competitor]” and its own product wins every single comparison, that’s not a review — that’s marketing wearing a review’s clothing.

Setting that aside, here is what the product actually claims to offer, and where it appears to differentiate itself meaningfully.

How it works: Credit Booster AI positions itself as a hybrid between a dispute tool and a credit coach. It pulls reports from all three bureaus (unlike Dovly’s TransUnion focus), identifies errors, and generates FCRA-compliant dispute letters. Where it differentiates is in a predictive coaching layer: the platform reportedly provides impact estimates for specific items (“this collection is suppressing your score by approximately 35 points — prioritize disputing it”), giving users a ranked action list rather than just a list of problems.

Pricing: The company lists pricing in the $19–$99 per month range depending on tier, with the basic coaching tier at the lower end and a premium plan with more hands-on review at the higher end. This is in line with competitors once you account for features.

What’s promising: The three-bureau coverage is a real advantage over Dovly. The coaching model — helping users understand why certain actions matter and in what order — is also more useful than pure automation for people who want to understand their credit profile, not just outsource the repair process.

What to watch: There is a notable absence of independent third-party reviews. The platform’s own content makes significant statistical claims (65-point average boosts, 65% success rates) that appear to be sourced from internal data or the company’s own test simulations rather than independent verification. The CFPB has noted, correctly, that no platform can guarantee score improvements, and any claims in that direction should be read carefully. The product looks interesting, but it hasn’t been on the market long enough for a truly trustworthy independent picture to emerge.

Best for: People who want three-bureau coverage and prefer a coaching-and-dispute hybrid over a pure automation product. Approach the marketing claims with appropriate skepticism and look for user reviews on Trustpilot or the App Store rather than on the company’s own domain.

The Honest Comparison Nobody Else Will Give You

Here’s the side-by-side breakdown without a recommended winner, because the right answer genuinely depends on your situation.

| Dovly | ChatGPT DIY | Credit Booster AI | ScorePivot | |

|---|---|---|---|---|

| Who it’s for | Individual consumers | Self-directed individuals | Individual consumers | Business operators |

| Bureau coverage | TransUnion only | All 3 (you pull reports) | All 3 | N/A (B2B) |

| Automation level | Moderate-high | None — you do everything | Moderate-high | High (for businesses) |

| Cost | Free / $40/mo or $100/yr | Free (ChatGPT Plus ~$20/mo) | ~$19–$99/mo | Subscription, 30-day trial |

| Tracking & monitoring | Yes | No | Yes | Yes (for clients) |

| Coaching / education | Basic | Strong (with right prompts) | Yes | Business-focused |

| Independent reviews | Yes, meaningful Trustpilot data | N/A | Limited | Limited |

| Main limitation | Single bureau, semi-manual | Time-intensive, no follow-up | Young product, self-reported data | Not a consumer product |

What None of Them Will Tell You

A few things are systematically underemphasized in this category:

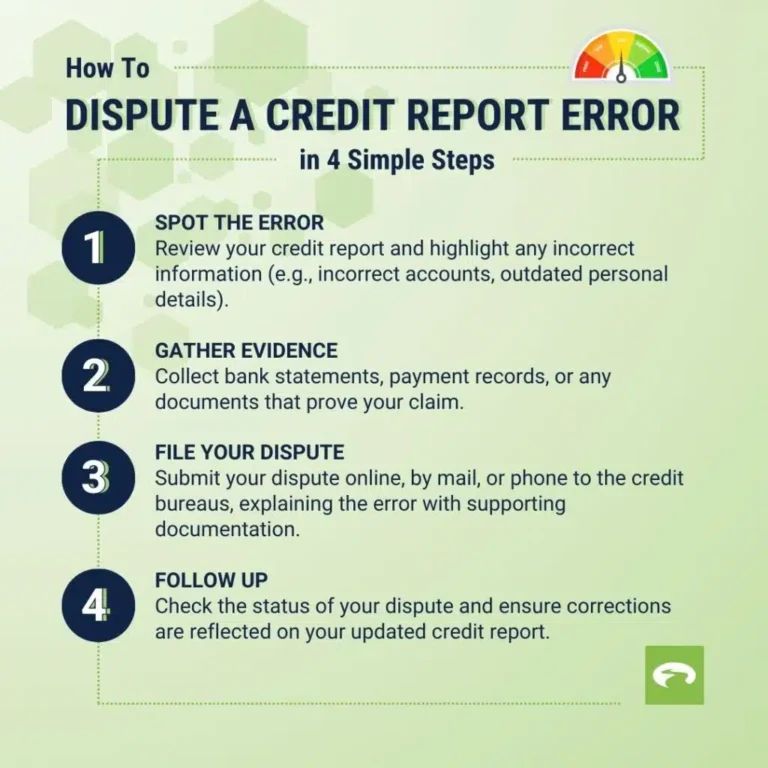

Disputing errors yourself is free. The FCRA gives you the right to dispute anything on your credit report directly with the credit bureaus at no cost. You can do this online at each bureau’s website. If you have a few specific errors and the patience to follow up, this is always an option — AI-assisted or not.

Credit bureaus have 30–45 days to investigate. After that, if they can’t verify the item, it must be removed. This timeline is the same whether you use Dovly, ChatGPT, or a traditional credit repair firm. No tool can speed up the bureau’s clock.

“Verified” items can be re-disputed. If a bureau says an item has been verified and you have documentation that contradicts this, you can dispute again. This is where persistence matters more than which software you use.

Data privacy is a real concern. Every one of these platforms — including ChatGPT — asks you to share sensitive personal financial information. Before uploading your credit report anywhere, read the privacy policy. Understand where your data goes and how long it’s retained.

Beware the “guaranteed results” language. Any service that guarantees a specific point increase is either lying to you or being recklessly loose with words. Results genuinely vary based on your individual report, the types of errors present, and how creditors respond to disputes.

Our Recommendation Top 5 Credit Repair Companies

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

The Bottom Line

If you want the simplest starting point for free, pull your reports from AnnualCreditReport.com, paste relevant sections into ChatGPT, and ask it to identify potential FCRA violations and draft customized dispute letters. It costs nothing, it works if you follow through, and it gives you a real understanding of what’s on your report.

If you want a structured product that handles the submission process for you and have primarily TransUnion issues, Dovly’s free tier is worth trying before you pay anything. Premium is reasonably priced if you’re seeing results.

If you want three-bureau coverage with a coaching overlay, Credit Booster AI is worth evaluating — but read independent reviews rather than the company’s own comparison pages, and hold the marketing claims loosely until the product has more time on the market.

And if someone is pitching you ScorePivot as a way to fix your personal credit, walk away. It’s a business operations product, and the confusion between the two is not accidental.

The credit repair industry has been built on information asymmetry — the idea that the process is too complicated for regular people to navigate alone. AI tools are genuinely starting to erode that advantage. But they work best when you understand what they’re actually doing, and when you go in with realistic expectations about what any software can and cannot change about your financial history.

The credit reporting laws referenced in this article — the Fair Credit Reporting Act and the Credit Repair Organizations Act — are federal U.S. laws. Always review current CFPB guidelines and consult a financial advisor or attorney for advice specific to your situation.