How to Dispute Credit Report Errors in 2026

You have the right to dispute any inaccurate information on your credit report. Correcting these errors usually involves reaching out to both the credit bureau and the company that originally reported the information. Once a dispute is submitted, both parties are required to investigate the issue and update your report if the information is found to be incorrect or cannot be verified.

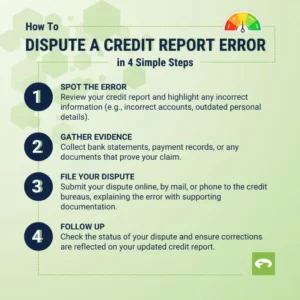

Dispute the information with the credit reporting companies

If you find an error on your credit report, the first step is to dispute it directly with the credit bureaus—Experian, Equifax, and/or TransUnion. It’s important to clearly explain what information you believe is incorrect, why it is wrong, and include any supporting documents that back up your claim.

When submitting a dispute by mail, make sure your letter includes your full contact details, such as your name, address, and phone number. If available, add your credit report confirmation number to help speed up the process.

Be sure to list each item you are disputing, along with the account number linked to it. Clearly describe the issue and state whether you want the information corrected or completely removed. It also helps to include a copy of your credit report with the disputed items highlighted or circled.

Always attach copies (never originals) of any documents that support your case. This could include payment records, settlement letters, or other proof that the information is incorrect.

For added security, you can send your dispute letter through certified mail and request a return receipt. This gives you proof that your letter was received and is being processed.

You can also submit disputes online or by phone through the official websites of the nationwide credit bureaus.

Equifax

Online: https://www.equifax.com/personal/credit-report-services/credit-dispute/

By phone or mail: Call the phone number shown on your credit report or call (866) 349-5191. Visit www.equifax.com/personal/contact-us/ to find the current address you can mail your dispute to.

Experian

Online or by mail: www.experian.com/disputes/main.html to dispute online or get instructions for how to remove dispute by mail.

By phone: Call the phone number shown on your credit report or call (888) 397-3742.

TransUnion

Online: dispute.transunion.com

By mail or phone: Visit www.transunion.com/credit-disputes/dispute-your-credit/mail-or-phone for instructions on how to Remove dispute by mail or phone, Call (800) 916-8800, Monday – Friday 8 a.m. 11 p.m. ET, Saturday and Sunday 8 a.m. – 5 p.m. ET to dispute over the phone.

When you submit a dispute, the credit reporting company is required to take action. They will investigate your claim, share all the relevant details you provided with the company that originally reported the information, and then inform you of the outcome once the review is complete.

However, not every dispute goes through a full investigation. If the credit bureau believes your request is incomplete, unclear, or lacks enough supporting details, they may decide it is “frivolous” or irrelevant. In such cases, they are not required to investigate further.

If this happens, the credit bureau must notify you in writing, explaining why your dispute was not processed. This notice must be sent within five business days after their decision, giving you a chance to correct or resubmit your request with the necessary information.

Then, dispute the information with the company that provided it to the credit reporting companies

Credit reporting companies collect your financial information from sources known as “furnishers.” These are businesses you already deal with, such as your bank, landlord, credit card issuer, or loan provider.

If you notice incorrect information on your credit report that came from one of these furnishers, you have the right to dispute it directly with them. It’s best to send your dispute in writing, and using certified mail is recommended so you have proof it was received. You can usually find the furnisher’s contact address on your credit report, or they may provide a specific address for handling disputes.

Once your dispute is submitted, the furnisher is generally required to investigate your claim and respond within 30 days. During this time, they will review the information you provided and check their records.

If they find that the information is inaccurate or cannot be verified, they must correct it or remove it entirely. After making changes, they are also required to notify all credit bureaus so your credit report can be updated accordingly.

However, if the furnisher determines that the information is accurate, it will remain on your credit report. In this case, you still have options—you can request that the credit bureaus add a statement to your report explaining that you dispute the item. This statement becomes part of your credit file and may be shared with lenders or anyone who checks your credit in the future.

How to Get Your Credit Report Before You Dispute Anything

Before you can dispute an error, you need to actually see your credit report. Many people skip this step and go straight to contacting the bureaus without knowing exactly what’s on their report — which leads to vague, ineffective disputes.

The only federally authorized source for your free credit report is AnnualCreditReport.com. You are legally entitled to one free report from each of the three bureaus — Equifax, Experian, and TransUnion — every 12 months. Pull all three, because errors don’t always appear on every bureau’s report. An account incorrectly reported as delinquent might only show up on one of them.

Once you have your reports, go through each one carefully. Look at every account, every balance, every payment status, and every personal detail. Take notes on anything that doesn’t look right. The more specific you are when you submit your dispute, the more seriously it gets treated.

Common Credit Report Errors You Should Be Looking For

Not everyone knows what a credit report error actually looks like. Here are the most common types of mistakes that appear on credit reports — and that you have every right to dispute:

Wrong personal information. Your name spelled incorrectly, a wrong address, an old phone number listed as current, or even someone else’s information mixed into your file. These seem minor but can cause real problems, especially if you share a similar name with a family member or someone with bad credit.

Accounts that don’t belong to you. If you see a credit card, loan, or collection account that you never opened, this could be a data error — or it could be a sign of identity theft. Either way, it needs to be disputed immediately.

Duplicate accounts. Sometimes the same debt gets listed twice, making it look like you owe twice as much as you actually do. This is more common than people realize, especially after a debt has been sold to a collection agency.

Incorrect payment status. An account marked as late or delinquent when you actually paid on time is one of the most damaging errors possible. Even a single incorrectly reported missed payment can drop your score significantly.

Wrong account balances or credit limits. If your reported balance is higher than it actually is, or your credit limit is listed as lower than it really is, your credit utilization ratio looks worse than it should — which directly hurts your score.

Accounts still showing as open after being closed. If you closed a credit card years ago and it’s still listed as active, that can skew your profile in ways that don’t reflect reality.

Negative items past their expiration date. Most negative items must be removed from your credit report after seven years. A bankruptcy can remain for up to ten years, but nothing negative should stay beyond that. If you see outdated items still on your report, they must come off.

Step-By-Step: How to Write an Effective Dispute Letter

Many disputes fail not because the error isn’t real, but because the letter isn’t written clearly enough. Here is exactly what your dispute letter needs to include to give it the best chance of success:

Step 1 — Your personal details at the top. Include your full legal name, current address, date of birth, and Social Security number. This helps the bureau match your letter to the right credit file without confusion.

Step 2 — Identify the error clearly. State the name of the account, the account number, and the specific information that is wrong. Don’t be vague. Instead of saying “this account is wrong,” say “this account shows a missed payment in March 2024, but I paid on time and have the bank statement to prove it.”

Step 3 — State exactly what you want done. Tell the bureau whether you want the information corrected or removed entirely. Be direct and specific.

Step 4 — List your supporting documents. Reference every document you are attaching — bank statements, payment receipts, settlement letters, court documents, or any other evidence. Always send copies, never your originals.

Step 5 — Sign and date your letter. An unsigned letter can be dismissed. Always sign it and include the date you’re sending it.

Keep a copy of everything you send. If you use certified mail, attach the receipt to your copy so you have a complete paper trail.

What Happens After You Submit a Dispute — And What to Do Next

Many people submit a dispute and then don’t know what to expect. Here is the full picture of what happens after your letter is received.

Once the credit bureau receives your dispute, they are required under the Fair Credit Reporting Act (FCRA) to complete their investigation within 30 days. In some cases where you provide additional information during the investigation, they may extend this to 45 days.

During this time, the bureau contacts the furnisher — the company that originally reported the information — and asks them to verify it. If the furnisher cannot verify that the information is accurate within the timeframe, the bureau must correct or delete it.

Once the investigation is complete, the bureau must send you written results. If the dispute results in a change, you are entitled to a free updated copy of your credit report showing the correction.

What if your dispute is rejected or comes back “verified”?

This is where many people give up — but you still have options. If the bureau says the information was verified and will remain on your report, you can:

- Request that a 100-word consumer statement be added to your credit file explaining your side of the dispute. Lenders will see this when they pull your report.

- Dispute directly with the original furnisher if you haven’t already done so, providing stronger documentation.

- File a complaint with the Consumer Financial Protection Bureau (CFPB) at ConsumerFinance.gov if you believe the bureau did not properly investigate your claim.

- Consult a consumer law attorney. If the bureau or furnisher is reporting information they know is inaccurate, you may have legal recourse under the FCRA.

Do not assume a rejected dispute is the end of the road. Persistence, stronger documentation, and knowing your legal rights often lead to a different outcome on a second submission.

Frequently Asked Questions About Disputing Credit Report Errors

Will disputing an error hurt my credit score?

No. Filing a dispute does not affect your credit score in any way. The investigation process is completely separate from score calculations.

Can I dispute multiple errors at the same time?

Yes, you can dispute multiple items in a single letter. However, be clear and organized — list each item separately with its own account number and explanation. Submitting everything in a jumbled way makes it easier for the bureau to label your dispute as frivolous.

Should I dispute online or by mail?

Both methods are legally valid. Disputing online is faster and more convenient. Disputing by certified mail gives you a stronger paper trail and is often recommended when the error is serious or when you’ve already had a dispute rejected once.

How long do errors stay on my credit report if I don’t dispute them?

Most negative items remain for seven years. Bankruptcies can stay for up to ten. However, if an item is inaccurate, it should never be on your report regardless of age — which is exactly why disputing errors matters.

Can a credit repair company dispute errors on my behalf?

Yes. Reputable credit repair companies handle the entire dispute process for you — writing letters, tracking responses, and following up with bureaus. This can be helpful if you’re dealing with multiple errors or if previous DIY disputes have been unsuccessful.