Credit Repair for the Clueless 2026

If you’re new to credit card repair, there’s no need to panic. It may sound complicated at first, but once you understand the basics, it becomes much easier to manage. Many people assume that simply paying bills on time is enough to maintain a good credit score. While that is an important factor, life can sometimes get in the way—unexpected expenses, financial hardship, or missed payments can all lead to the need for credit repair.

Everyone wants a strong credit profile, so the more you understand how credit repair works, the better prepared you are to protect your financial future.

At the moment, the economy is challenging, and lenders are more cautious than ever. Credit card companies are tightening their approval rules, making it harder for people with poor credit or high debt to access new loans or credit. That’s why it’s more important than ever to manage your credit responsibly and take action early if things start to go off track.

Understanding Your Credit Score

Your credit score is not just a number—it reflects your financial behaviour and responsibility. Several factors influence it, including your payment history, outstanding debt, credit usage, and account activity. Improving your score requires both responsible financial habits and time.

One way some people improve their credit profile is by becoming an authorized user on a trusted family member’s credit card account. When managed responsibly, this can positively impact your credit report, as it shows that a lender trusts you with credit access.

Reviewing Your Credit Reports

It’s also important to regularly check your credit reports from the major credit bureaus. These reports give you a clear picture of your financial standing and help you identify any errors, outdated information, or problem areas that may be lowering your score.

Knowing exactly where you stand allows you to plan better, take control of your finances, and work step by step toward rebuilding your credit. If you’ve faced financial challenges or maxed out credit cards, reviewing your report is the first step toward recovery and long-term financial stability.

Communicating with Creditors and Collection Agencies

When dealing with credit repair, one of the most important steps is keeping communication open with your creditors and collection agencies. Instead of ignoring calls or avoiding contact, it’s better to stay honest and responsive. Showing a willingness to cooperate often makes it easier to find workable repayment solutions.

In many cases, collection agencies may be open to negotiating payment plans based on what you can realistically afford. Avoiding them completely can make the situation worse and may further damage your credit history. Remember, the goal is to rebuild your credit—not make things harder for yourself.

Protecting Yourself from Identity Theft

Identity theft is another serious issue that can negatively impact your credit. Sometimes, individuals discover that accounts or purchases were made in their name without their permission, leaving them responsible for debts they did not create.

To protect yourself, always safeguard your personal and financial information. Regularly checking your credit reports helps you quickly spot any suspicious activity. If you find unauthorized charges or accounts, report and dispute them immediately with the credit bureaus and the relevant financial institutions.

Knowing Your Legal Rights

It’s also important to understand your rights when dealing with creditors and collection agencies. Being informed about consumer protection laws can help you avoid unfair practices and ensure that you are treated fairly throughout the credit repair process.

When you know your rights, you are in a stronger position to handle disputes and protect your financial interests confidently.

DIY Credit Repair vs. Paid Services

If you’re planning to repair your credit, it’s worth considering whether you truly need to pay a company for assistance. Many people successfully manage credit repair on their own by reviewing their credit reports, disputing errors, and communicating directly with creditors.

In some cases, paid services may not be necessary, and doing it yourself can save money that could instead be used to pay down existing debts. However, it’s important to do proper research and stay cautious to avoid scams or unrealistic promises.

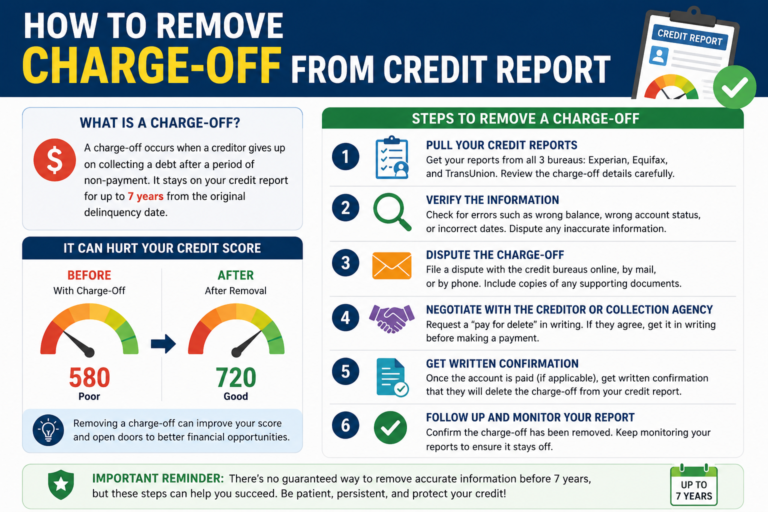

How Long Does Credit Repair Actually Take?

One of the most common questions beginners ask is: how long will this take? The honest answer is — it depends. Minor issues like a single late payment or a small collection account may begin showing improvement within 30 to 90 days once addressed. However, more serious negative marks such as bankruptcies, foreclosures, or multiple charge-offs can take anywhere from two to seven years to fully age off your credit report.

That said, you don’t have to wait years to see meaningful improvement. Many people notice a noticeable score increase within three to six months simply by paying down balances, disputing errors, and keeping accounts in good standing. The key is consistency — small, steady actions done repeatedly over time produce real results.

Understanding this timeline helps you set realistic expectations and stay motivated rather than feeling discouraged when change doesn’t happen overnight.

The Role of Credit Utilization — and Why It Matters More Than You Think

Many people focus entirely on missed payments when thinking about their credit score, but credit utilization is one of the most powerful and fastest-moving factors you can control. Credit utilization refers to how much of your available credit limit you are currently using. For example, if you have a credit card with a $1,000 limit and you’ve spent $700 on it, your utilization rate is 70% — which is considered very high.

Experts generally recommend keeping your utilization below 30% across all your credit cards, and ideally below 10% if you want the best possible score. If your cards are currently maxed out or close to it, paying them down — even partially — can result in a quick and significant score boost once the updated balance is reported to the credit bureaus.

This is one of the fastest DIY wins available in credit repair, and it costs nothing except discipline.

What to Do If a Creditor Won’t Cooperate

Sometimes, despite your best efforts to communicate and negotiate, a creditor or collection agency may not be willing to work with you. In these situations, you still have options. If the debt is genuinely yours and valid, you may want to consider sending a written goodwill letter — a polite, professional request asking the creditor to remove or update the negative mark as a gesture of goodwill, especially if you’ve since paid the account or have a history of otherwise good payments.

If the negative item on your report is inaccurate, incomplete, or unverifiable, you have the legal right to formally dispute it with the credit bureaus under the Fair Credit Reporting Act (FCRA). The bureau is then required to investigate the claim within 30 days. If the creditor cannot verify the information, the item must be removed or corrected.

Document every communication — keep records of letters sent, responses received, and dispute submissions. A paper trail protects you and strengthens your case.

Building New Positive Credit While Repairing Old Damage

A mistake many people make during credit repair is focusing only on the negative and forgetting to build positive history at the same time. Both matter. While removing or resolving negative items improves your score, adding new positive accounts actively works in your favor too.

If you currently have no open accounts or very limited credit, a secured credit card can be an excellent starting point. With a secured card, you deposit a small amount as collateral — typically between $200 and $500 — and that becomes your credit limit. Use it lightly each month and pay the balance in full, and within six to twelve months you’ll have established a new, positive payment history.

Credit builder loans, offered by many credit unions and online lenders, work similarly. You make small monthly payments that are reported to the credit bureaus, helping you demonstrate responsible borrowing behavior. Over time, this combination of removing negatives and adding positives creates a well-rounded credit profile.

When to Consider Professional Help

There is no shame in asking for help, and certain situations do genuinely benefit from professional guidance. If you are dealing with a large volume of negative items, suspected identity theft, creditor harassment, or legal complications such as wage garnishment or lawsuits from debt collectors, a reputable credit repair company or a nonprofit credit counselor may be worth consulting.

Look for companies accredited by recognized consumer protection bodies, and always read reviews carefully before signing any agreement. Legitimate services will never guarantee specific results or charge large upfront fees before performing any work.

The most important thing is to keep moving forward — taking even one small action today puts you ahead of where you were yesterday.