How to Remove Late Payments from Your Credit Report (And Actually Get Results)

Here is Complete Guide How to Remove late payments and improve credit.You checked your credit report. There it is — a late payment, sitting like a stain on an otherwise decent history. Maybe it was a single missed bill during a chaotic month. Maybe a payment got lost in the mail. Maybe you genuinely didn’t know the balance existed. Whatever the reason, you’re here now, and you want it gone.

The good news? Removing late payments from your credit report is entirely possible in many cases. The process takes patience, persistence, and knowing which lever to pull — but people do it every day. This guide walks you through every real method available, in plain language, without sugarcoating what works and what doesn’t.

Why Late Payments Hurt So Much

Before we talk strategy, it helps to understand what you’re actually dealing with.

A single late payment — defined as 30 or more days past due — can drop your credit score by 60 to 110 points depending on your starting score and overall profile. The higher your score, the harder the fall. And that drop doesn’t fade quickly. Under federal law, a late payment can legally remain on your credit report for up to seven years from the date of the original delinquency.

Seven years is a long time to carry baggage from one bad month.

The three major credit bureaus — Equifax, Experian, and TransUnion — each maintain their own version of your credit history. A late payment reported by a lender gets picked up by all three, which means the damage is tripled. This is also important to remember when you’re trying to fix things: you may need to dispute with all three bureaus separately.

Remove late payments and improve credit

Method 1: Dispute Inaccurate Information

This is the most powerful tool you have — and it’s completely free to use.

The Fair Credit Reporting Act (FCRA) gives you the right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. If a late payment was reported in error, you are legally entitled to have it removed.

What counts as an error?

More than you’d think. Common mistakes include:

- The payment was on time, but the creditor reported it late

- The date of the late payment is wrong

- The account doesn’t belong to you (identity theft or mixed files)

- The same late payment is listed multiple times

- The amount or account number is incorrect

- The late payment is older than seven years but still appearing

How to file a dispute:

Start by pulling your free credit reports from AnnualCreditReport.com. Read through every account carefully. When you find an error, you have three options: dispute online through each bureau’s website, dispute by phone, or dispute by certified mail.

Disputing by certified mail is the most effective method. It creates a paper trail, gives you time to organize your thoughts, and forces the bureau to take you seriously. Your letter should include your full name, address, date of birth, Social Security number, a clear explanation of what’s wrong, and copies (not originals) of any supporting documents.

Once you file a dispute, the bureau has 30 days to investigate. They contact the original creditor to verify the information. If the creditor can’t confirm the accuracy, the item must be removed. If the bureau finds the information is indeed accurate, the dispute is closed and the item stays — but you haven’t lost anything by trying.

Keep copies of everything. If your dispute is ignored or handled improperly, you have the right to escalate to the Consumer Financial Protection Bureau (CFPB) or consult an FCRA attorney.

Method 2: Goodwill Deletion

Here’s the method no one talks about enough: just asking.

If the late payment is accurate — you really did pay late — you can still try to have it removed by appealing to the creditor’s goodwill. This sounds too simple to work, but it succeeds more often than you’d expect, particularly if you’ve been a loyal customer with a solid overall payment history.

A goodwill letter is a written request to the creditor (not the credit bureau) asking them to remove the negative mark as a gesture of goodwill. You’re not disputing the accuracy. You’re acknowledging what happened and asking for a second chance.

What makes a goodwill letter work:

The key is making it personal and genuine. Explain the circumstances that led to the late payment — a medical emergency, job loss, family crisis, or simple oversight. Show that it was out of character for you. Point to your payment history before and after the incident. Express that you’ve since gotten back on track.

You’re appealing to a human being on the other end who has the authority to update the account. Some creditors have explicit policies against goodwill deletions. Others leave it to the discretion of customer service representatives. You won’t know until you try.

Tips for a stronger goodwill letter:

Send it via certified mail to the creditor’s executive customer service team, not the general address. Keep the tone respectful and humble. Be specific — vague letters get ignored. And follow up. One letter often isn’t enough. Some people send the same goodwill request three or four times before getting a yes.

Timing matters too. If the account is still open and you’re a current customer in good standing, your leverage is higher. Creditors value ongoing relationships and may be more willing to accommodate a long-term customer.

Method 3: Pay-for-Delete Negotiation

If you have a collection account with a late payment attached, you may have room to negotiate a pay-for-delete agreement. This is exactly what it sounds like: you offer to pay the debt in full (or settle for a negotiated amount) in exchange for the collection agency removing the negative item from your credit report.

This approach is more common with third-party debt collectors than with original creditors, and it’s important to get any agreement in writing before you pay a single dollar. If you pay without written confirmation of the deletion promise, the collector has no legal obligation to remove anything.

A pay-for-delete agreement does not work on every account. Some debt collectors refuse on principle. Others will agree readily because they want the money. Approach the conversation matter-of-factly: “I’m prepared to settle this account today if we can agree that the tradeline will be removed from all three credit bureaus upon receipt of payment.”

Be aware that even if the collection account is removed, the original late payment from the original creditor may still appear separately. You may need to address both entries.

Method 4: Work with the Original Creditor Directly

Many people focus on the credit bureaus when the real leverage is with the lender or creditor who reported the late payment in the first place.

Credit bureaus don’t create the information on your report — they receive it from creditors. If you can get the creditor to update or retract the information, the bureau has an obligation to reflect that change.

Call the creditor’s customer service line and ask to speak with someone in the credit reporting department. Be polite and direct. Explain your situation, reference your history with them, and ask if there’s anything they can do to update the reporting. Some creditors have internal hardship programs that allow for courtesy removals on a first-time basis.

If you financed a car, have a mortgage, or carry a credit card you’ve held for years, you have relationship equity. Use it.

Method 5: Wait It Out (With a Plan)

Sometimes, despite your best efforts, the late payment stays. It’s accurate, the creditor won’t budge, and your disputes have been closed.

In that case, time becomes your strategy.

Late payments do the most damage in the first two years. After that, their impact on your score gradually decreases as newer, positive information begins to outweigh them. By year four or five, a single old late payment has relatively little weight — especially if you’ve been building a strong, consistent payment history since then.

Set up autopay on every account. Keep your credit utilization below 30%. Don’t apply for too much new credit at once. These habits won’t erase the past, but they will actively build the future. And your future credit profile is what lenders will ultimately be looking at.

What Not to Do

A few warnings worth taking seriously:

Don’t pay a credit repair company to do what you can do yourself. Every legal method available to a credit repair company is available to you at no cost. Many companies charge hundreds or thousands of dollars for the same dispute letters you can write for free. Some cross into outright fraud. The FTC has taken action against many of these companies.

Don’t file frivolous disputes hoping things slip through. Disputing accurate information you know to be correct is not only likely to fail — it can flag your file and make future legitimate disputes harder.

Don’t close accounts after a late payment. Closing an account reduces your available credit and can shorten your credit history, both of which hurt your score independently.

Don’t assume silence means acceptance. If you don’t hear back after a dispute or goodwill letter, follow up. Persistence is often the difference between a yes and a no.

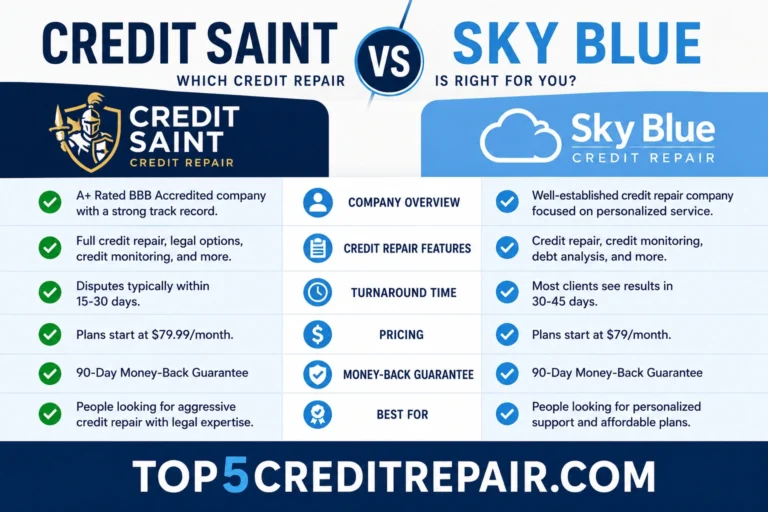

Our Recommendation Top 5 Credit Repair Companies

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

The Bottom Line

Late payments are serious, but they’re not permanent — and even when they can’t be removed immediately, they can be actively managed. Start with your free credit reports, look for errors you can dispute, and then decide whether a goodwill letter or direct creditor negotiation makes sense for your situation.

You don’t need a law degree. You don’t need to pay someone else. You need your facts straight, your tone respectful, and the willingness to follow through.

Your credit history belongs to you. Take ownership of it.