Credit Repair vs Credit Counseling — What’s the Difference?

Good credit opens doors that bad credit keeps shut. Better interest rates on homes, cars and credit cards. Lower insurance premiums. Easier approval for rental apartments and utilities. And in some cases, even better job opportunities.

People struggling with bad credit understand this all too well. They also know that improving their credit is possible — they just need the right path to get there.

That’s where credit counseling and credit repair come in. Both offer a way into the “good credit club,” but make no mistake — these are two very different roads leading to the same destination.

The one thing they share? Both work toward cleaning up your credit report. Neither can erase legitimate negative marks like late or missed payments — those are accurate and they stay. But both can challenge unfair blemishes — things like identity theft, billing errors, or accounts wrongly sent to collections through no fault of your own.

How they go about doing that, though, is a completely different story.

And here’s the part most people overlook — not every company operating in this space has your best interests at heart. Some are legitimate. Others? Not so much.

So before you knock on any door, make sure you know exactly what’s waiting on the other side.

Here is Complete Guide about Credit Repair vs Credit Counseling

How Do I Recognize a Credit Counselor?

Not sure if you’re dealing with a legitimate credit counselor? Here are the signs to look for.

- A real credit counselor typically works for a nonprofit organization. They sit down with you — or connect with you online or by phone — and focus on helping you understand your money, not just your debt. They’ll help you build a realistic budget and put together a structured repayment plan that actually fits your situation.

- When it comes to your creditors, they work on your behalf to set up a payment arrangement — and in many cases, they can get creditors to pause collection efforts and waive late fees while you’re on the plan. The focus is on making your monthly payments more manageable, not on reducing what you actually owe.

- And here’s one of the clearest signs you’re working with someone legitimate — they will never tell you to stop paying your debts. That’s a red flag that belongs to a very different kind of company.

Debt Settlement

Debt settlement companies promise to negotiate your debts down for a fee. The basic idea is that you save up a lump sum, they approach your lenders or collectors, and try to settle for less than what you owe.

Here’s something important to understand upfront — any money you set aside in a savings account for this purpose still belongs to you. That account must be managed by an independent third party, and you have the right to withdraw from it at any time, no penalties attached. In reality though, many of these companies treat that money as their fees rather than funds to actually settle your debts.

Before You Sign Anything, Know This:

- Many lenders simply won’t negotiate with debt settlement companies

- Most lenders and collectors already have standard policies on how much they’ll forgive — your individual situation may not change that

- A debt settlement company rarely gets you a better deal than you could negotiate yourself

- They cannot guarantee how much you’ll save or how long the process will take

- They cannot wipe out all your debts — period

How Do You Spot a Debt Settlement Company?

- Usually a for-profit business that charges for its services

- Offers to negotiate settlements with your lenders or collectors

- Typically has no pre-existing agreements with lenders

- Works toward paying off debts through a lump sum

- Almost always advises you to stop paying creditors while negotiations are ongoing — which means fees and interest keep piling up, your credit takes more damage, and you become more vulnerable to lawsuits

- May try to get portions of your debt forgiven, which can create a tax bill on the forgiven amount

Watch Out for Upfront Fees

A debt settlement company is likely breaking the law if they charge you before all three of these things happen:

- They successfully renegotiated, settled or changed the terms of at least one of your debts

- You reviewed and agreed to the settlement they reached with your creditor

- You made at least one payment to the creditor as a result of that agreement

If a company asks for money before hitting these milestones — walk away.

And if you truly cannot afford to pay what you owe, bankruptcy may be worth exploring. Speaking with a bankruptcy attorney can help you understand whether that path makes sense for your situation.

Debt Consolidation Loans

Banks, credit unions and other lenders offer debt consolidation loans as another option. The concept is simple — you borrow one lump sum to pay off all your existing debts, then make a single monthly payment going forward. It’s cleaner, easier to manage, and sometimes comes with a lower interest rate than what you’re currently paying.

But Before You Go This Route:

- That low interest rate may be a teaser rate — a temporary offer that expires and leaves you with higher payments later

- A lower monthly payment might just mean you’re stretching repayment over a longer period

- When you factor in the loan’s full length, fees and total cost, you may end up paying more in the long run than if you had stuck with your original payments

Understanding Credit Counseling

Credit counseling helps people get a better handle on their money. It covers budgeting, managing debt and building smarter financial habits — all with one simple goal: helping you stay out of debt for good.

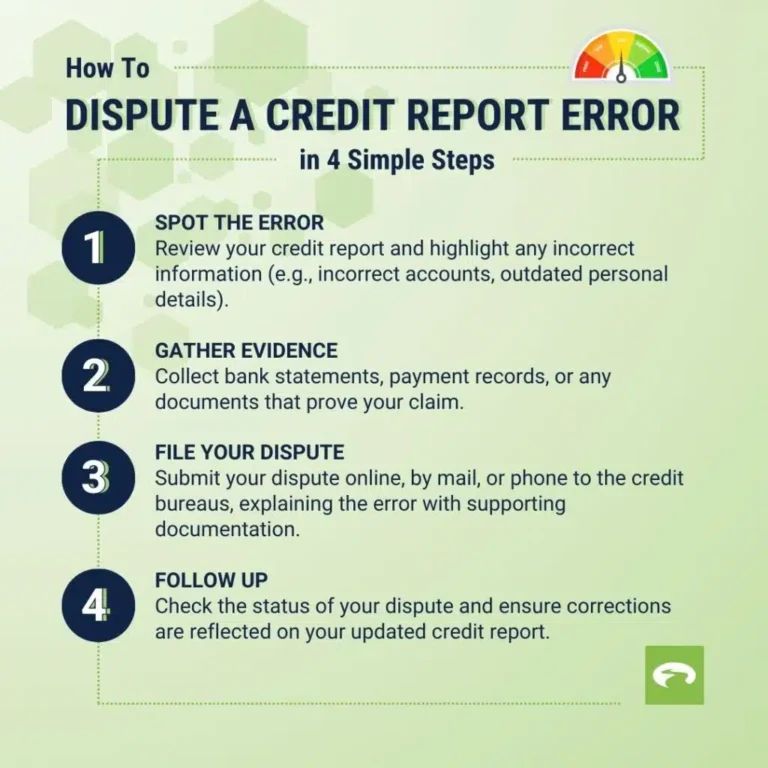

Counselors dig into your full financial picture. They review your credit report, explain what’s hurting your score and help you figure out the best way to pay down what you owe. If there are errors on your report, they’ll walk you through how to get them fixed.

Beyond that, they can help with:

- Building a monthly budget that actually works

- Navigating the home buying process

- Sorting out student loan options

- Deciding whether bankruptcy makes sense

- Planning ahead for retirement

- Breaking down the differences between debt management, debt settlement and debt consolidation

As for cost — it depends on where you live. Every state regulates the industry differently, so pricing varies. Nonprofit agencies generally offer counseling for free, though if you sign up for a debt management program, expect an average enrollment fee of around $52 and a monthly fee of about $34.

The Pros

- Counselors are trained and certified in credit reports, debt and personal finance

- They help you budget better so you don’t sink deeper into debt

- Nonprofits are required by law to put your interests first

- Sessions are available online, by phone or in person

- They provide educational resources for just about any debt situation

The Cons

- The free counseling is great, but debt management programs come with fees

- One session might help some people, but if you’re deep in debt, full programs typically take 3 to 5 years to complete

Understanding Credit Repair

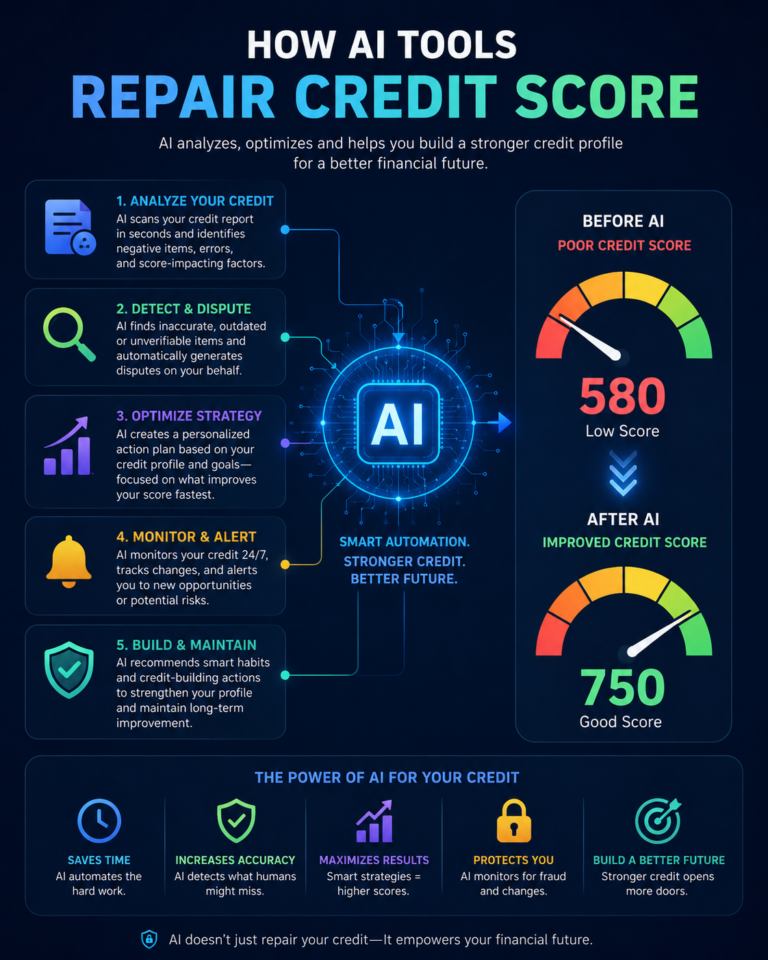

The idea behind credit repair sounds straightforward — find the negative, inaccurate items dragging down your credit score and get them removed. Simple enough, right?

Not exactly.

Here’s the reality: most of the negative marks on your credit report are there for a reason. They’re accurate. And no one — not you, not a credit repair company, not anybody — can legally remove information that’s correct and current.

That said, errors do exist. The Consumer Financial Protection Bureau estimates that roughly 20% of credit reports contain mistakes. That’s around 40 million Americans walking around with correctable errors on their reports without even knowing it. Credit repair companies argue that fixing those errors is exactly what they do best.

Their process starts with pulling your full credit report and going through every single negative item to see what holds up and what doesn’t. Services typically include:

- Confirming your name, address and Social Security number are accurate

- Checking whether late or missed payments were reported correctly

- Verifying charge-offs, bankruptcies and tax liens

- Validating debts from collection agencies

- Sending cease-and-desist letters to stop collection calls

- Building disputes for errors found on your report

Now let’s talk money. Pricing in this industry is all over the place. Most companies charge a monthly fee somewhere between $75 and $150, plus a setup fee that can run anywhere from $50 to $200. Some charge per item removed. Either way, there’s rarely a clear finish line — you could be paying for months without knowing when it ends.

If you go this route, get the full fee schedule in writing. Understand exactly what you’re being charged for and whether there’s a cancellation penalty before you sign anything.

How Do I Recognize a Credit Repair Company?

Knowing what to look for can save you a lot of money and frustration. Here are the telltale signs you’re dealing with a credit repair company:

- They’re almost always for-profit and charge a fee for their services

- They promise fast results — a quick boost to your credit score sounds appealing, but it’s rarely realistic

- They offer to remove negative items from your credit reports across all three major bureaus — Experian, Equifax and TransUnion

- They typically charge a monthly fee, often justified by repeatedly disputing the same negative items on your report

Watch Out for Monthly Subscription Fees

A lot of credit repair companies use telemarketing to bring in clients. If a company signed you up through a telemarketing call, the law is clear — they cannot bill you or collect any payment until two specific things happen:

- The timeframe they promised to deliver results has fully passed. This means no upfront fees and no ongoing monthly charges during that period. Some companies try to sidestep this by calling it a “subscription fee” — but the label doesn’t change the rule.

- They have sent you an actual report from a consumer reporting agency showing that they delivered the results they promised — and that report must be dated at least six months after those results were achieved.

If a company asks for payment before both of these conditions are met, that’s a serious red flag.

The Pros

- Forces you to actually look at your credit report and understand it

- Can remove negative marks that don’t belong there

- May catch billing errors you weren’t even aware of

- Experienced at disputing mistakes with creditors and bureaus

The Cons

- You can do this yourself — disputing errors doesn’t require paying someone else

- Credit repair scams are rampant in this industry, and government agencies have flagged it repeatedly

- Costs can add up fast with no guaranteed results

- Nothing is promised — you may pay for months and see little improvement

Here is Our Recommendation top 5 Best Credit Repair companies

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Safeport Law – Best for Legal Support

- The Credit People – Best for Low Setup Fees

- Sky Blue Credit – Best Value

So Which One Should You Choose?

Honestly, the differences between credit counseling and credit repair make the decision easier than it looks.

Credit counseling teaches you how to manage money and avoid the financial habits that damage your credit in the first place. Credit repair tries to clean up the mess after the fact — and only some of it, at that. The honest truth is that most negative marks on a credit report can’t be touched because they’re accurate.

One more thing worth knowing: the Consumer Financial Protection Bureau took legal action against two of the biggest names in credit repair — Lexington Law and CreditRepair.com — for charging illegal upfront fees and using deceptive marketing to pull in clients. When the federal government goes after the industry leaders, that’s not a small warning sign.

Your safest bet? Find a reputable nonprofit credit counseling agency. It may take longer, and it requires real effort on your part, but it costs far less and leaves you genuinely better off — not just with a cleaner report, but with the knowledge to keep it that way.

FAQs:

How Long Does It Take to Improve Your Credit Score After Debt Settlement?

Honestly, there’s no single answer — it depends on where your credit stands right now and what your overall credit history looks like.

That said, here’s what most people don’t think about before going the debt settlement route. To get creditors to accept a lower payout, you typically have to stop making monthly payments first. Those missed payments don’t just disappear — they leave negative marks on your credit report that stick around for seven years.

Credit Repair vs Credit Counseling which one is better?

In our research Credit repair is better because you see errors on your credit report And also you don’t have the time or confidence to dispute errors yourself.

How Much Does Credit Repair Cost?

Credit repair pricing is pretty straightforward once you know what to expect. Most companies charge somewhere between $50 to $150 per month depending on the plan you go with. On top of that, many also charge a one-time setup fee upfront — usually around the same range as the monthly cost.

So before you commit, make sure you understand exactly what you’re signing up for and how long you’ll be paying for it.

How Much Does Consumer Credit Counseling Cost?

The good news — credit counseling is one of the more affordable options out there. Most agencies offer a free initial consultation where they review your full financial situation and walk you through your best options for managing debt. Many also throw in extras at no cost, like budgeting help and personal finance workshops.

If you need ongoing support beyond that, some agencies do charge a monthly fee — but it’s generally quite reasonable, typically falling somewhere between $20 and $75 per month.

Does credit counseling affect your credit score?

Simply meeting with a credit counselor won’t touch your credit score — the consultation itself has no impact whatsoever. However, depending on what steps you and your counselor decide to take after that meeting, things could shift. For example, enrolling in a debt management plan or closing certain accounts may have an effect on your score, for better or worse depending on your situation.