How to Dispute Credit Report Errors

You have the right to dispute any inaccurate information on your credit report. Correcting these errors usually involves reaching out to both the credit bureau and the company that originally reported the information. Once a dispute is submitted, both parties are required to investigate the issue and update your report if the information is found to be incorrect or cannot be verified.

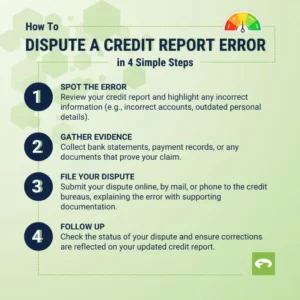

Dispute the information with the credit reporting companies

If you find an error on your credit report, the first step is to dispute it directly with the credit bureaus—Experian, Equifax, and/or TransUnion. It’s important to clearly explain what information you believe is incorrect, why it is wrong, and include any supporting documents that back up your claim.

When submitting a dispute by mail, make sure your letter includes your full contact details, such as your name, address, and phone number. If available, add your credit report confirmation number to help speed up the process.

Be sure to list each item you are disputing, along with the account number linked to it. Clearly describe the issue and state whether you want the information corrected or completely removed. It also helps to include a copy of your credit report with the disputed items highlighted or circled.

Always attach copies (never originals) of any documents that support your case. This could include payment records, settlement letters, or other proof that the information is incorrect.

For added security, you can send your dispute letter through certified mail and request a return receipt. This gives you proof that your letter was received and is being processed.

You can also submit disputes online or by phone through the official websites of the nationwide credit bureaus.

Equifax

Online: https://www.equifax.com/personal/credit-report-services/credit-dispute/

By phone or mail: Call the phone number shown on your credit report or call (866) 349-5191. Visit www.equifax.com/personal/contact-us/ to find the current address you can mail your dispute to.

Experian

Online or by mail: www.experian.com/disputes/main.html to dispute online or get instructions for how to remove dispute by mail.

By phone: Call the phone number shown on your credit report or call (888) 397-3742.

TransUnion

Online: dispute.transunion.com

By mail or phone: Visit www.transunion.com/credit-disputes/dispute-your-credit/mail-or-phone for instructions on how to Remove dispute by mail or phone, Call (800) 916-8800, Monday – Friday 8 a.m. 11 p.m. ET, Saturday and Sunday 8 a.m. – 5 p.m. ET to dispute over the phone.

When you submit a dispute, the credit reporting company is required to take action. They will investigate your claim, share all the relevant details you provided with the company that originally reported the information, and then inform you of the outcome once the review is complete.

However, not every dispute goes through a full investigation. If the credit bureau believes your request is incomplete, unclear, or lacks enough supporting details, they may decide it is “frivolous” or irrelevant. In such cases, they are not required to investigate further.

If this happens, the credit bureau must notify you in writing, explaining why your dispute was not processed. This notice must be sent within five business days after their decision, giving you a chance to correct or resubmit your request with the necessary information.

Then, dispute the information with the company that provided it to the credit reporting companies

Credit reporting companies collect your financial information from sources known as “furnishers.” These are businesses you already deal with, such as your bank, landlord, credit card issuer, or loan provider.

If you notice incorrect information on your credit report that came from one of these furnishers, you have the right to dispute it directly with them. It’s best to send your dispute in writing, and using certified mail is recommended so you have proof it was received. You can usually find the furnisher’s contact address on your credit report, or they may provide a specific address for handling disputes.

Once your dispute is submitted, the furnisher is generally required to investigate your claim and respond within 30 days. During this time, they will review the information you provided and check their records.

If they find that the information is inaccurate or cannot be verified, they must correct it or remove it entirely. After making changes, they are also required to notify all credit bureaus so your credit report can be updated accordingly.

However, if the furnisher determines that the information is accurate, it will remain on your credit report. In this case, you still have options—you can request that the credit bureaus add a statement to your report explaining that you dispute the item. This statement becomes part of your credit file and may be shared with lenders or anyone who checks your credit in the future.