Simple Steps in Doing Your Own Credit Repair in 2026

In today’s challenging economy, maintaining a good credit score is more important than ever. A strong credit profile shows lenders that you manage your finances responsibly by balancing your income, expenses, and debt obligations. However, missed payments, collection accounts, and reporting errors can negatively affect your credit standing and make it harder to qualify for loans, credit cards, or favorable interest rates.

That’s where credit repair comes in. The good news is that many credit issues can be addressed on your own without paying expensive fees to a credit repair company. In fact, some companies that promise instant credit repair or guaranteed credit score increases often fail to deliver on their claims. By learning the basics of credit repair, reviewing your credit reports, and disputing inaccurate information, you can take control of your financial future and work toward a healthier credit score.

Start by obtaining both digital and printed copies of your credit reports from the major credit bureaus. Understanding your current credit situation is the first step toward successful credit repair. By law, you can request a free credit report each year, so take advantage of this opportunity to review your credit history. You may also qualify for an additional free report if you’ve recently been denied credit, a loan, or another financial service.

Carefully reviewing your credit reports gives you a clear picture of your credit standing, including any errors, negative items, or areas that need improvement. With accurate information in hand, you can create a realistic plan to repair your credit and improve your score. Making financial decisions based on facts rather than guesswork can save time, reduce stress, and help you reach your credit goals more effectively.

Review your credit history carefully and take a close look at your spending habits. Make sure every account listed in your credit report actually belongs to you, because identity theft and fraudulent activity can sometimes appear without warning. If you notice anything suspicious or accounts that don’t seem familiar, you can dispute them with the credit bureaus through phone, email, or written request.

Once you’ve confirmed that all accounts are accurate and truly yours, focus on bringing everything up to date. Start by paying off overdue balances and settling accounts that have gone into collections, as these have a major negative impact on your credit score. Many collection agencies are open to negotiation, so it’s often possible to arrange a manageable payment plan. Taking care of these debts first helps clean up your credit profile and puts you in a stronger position to rebuild your financial health.

Bring your credit card balances down as much as possible, especially if they are maxed out. High credit utilization can significantly hurt your credit score, and improving it may take time—sometimes even a couple of years—depending on your overall financial situation. Focus on gradually paying down your balances and avoiding new unnecessary debt. Be cautious of companies that promise quick fixes for free or charge hidden fees, as some may not be legitimate.

Another helpful option is becoming an authorized user on a trusted family member’s credit card. If someone adds your name to an account with a good payment history, it can positively reflect on your credit profile and help build your creditworthiness over time.

Rebuilding credit is not something that happens overnight, especially during challenging economic times. However, with consistent effort, responsible spending habits, and steady repayment of debt, you can repair your credit on your own in a legal and effective way. Patience and discipline are key to seeing long-term financial improvement.

Our Recommendation:

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

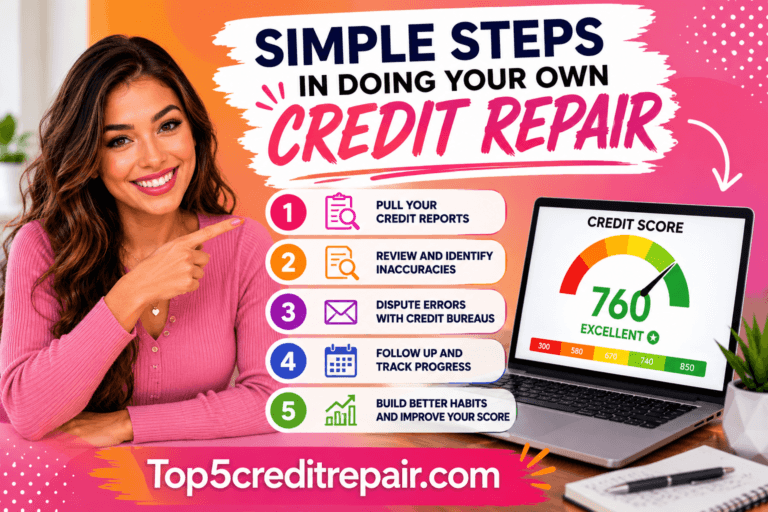

The 7 Simple Steps to Doing Your Own Credit Repair

Most people who try to repair their own credit fail not because the process is too hard, but because they don’t follow a clear order. Credit repair has a sequence. Skip a step or do things out of order and you waste months of effort. Here is exactly how to do it — from the very beginning to the point where you start seeing real results.

Step 1 — Pull All Three of Your Credit Reports

The first thing you need to do before anything else is get your hands on your actual credit reports. Not an estimate. Not a credit score app summary. Your full reports from all three bureaus — Equifax, Experian, and TransUnion.

The only place to get them for free without a credit card or hidden trial is AnnualCreditReport.com. This is the federally authorized source and it costs nothing. Pull all three at the same time because the same error doesn’t always show up on every bureau’s report. A collection account incorrectly listed as unpaid might appear on Equifax but not on TransUnion — so checking just one report means you could miss half the problem.

Once you have all three reports, print them or save them somewhere you can easily reference. You’re going to need them for the next steps.

Step 2 — Understand What Actually Makes Up Your Credit Score

Before you start making changes, you need to know what you’re actually trying to improve. Your credit score is calculated from five specific factors, each carrying a different weight:

- Payment History — 35% This is the biggest factor by far. Every on-time payment builds your score. Every missed or late payment damages it. Even one 30-day late payment can drop your score by 50 to 100 points depending on where you started.

- Credit Utilization — 30% This is how much of your available credit you are currently using. If your total credit limit across all cards is $5,000 and you owe $4,000, your utilization is 80% — which is very damaging. Keeping this below 30% helps significantly. Below 10% is ideal.

- Length of Credit History — 15% The longer your accounts have been open, the better. This is why closing old credit cards — even ones you don’t use — can sometimes hurt your score.

- Credit Mix — 10% Having a variety of account types (credit cards, installment loans, auto loans) shows lenders you can manage different kinds of credit responsibly.

- New Inquiries — 10% Every time you apply for new credit, a hard inquiry is placed on your report. Too many in a short period signals risk to lenders and can lower your score temporarily.

Knowing this breakdown helps you prioritize. If your utilization is at 75%, fixing that alone can produce a faster score boost than almost anything else you can do.

Step 3 — Identify Every Error on Your Reports

Now go through each report line by line. You are looking for anything that is wrong, outdated, or doesn’t belong to you. Here are the most common errors people find:

- Accounts you never opened

- Payments marked late when you paid on time

- Balances that are higher than what you actually owe

- The same debt listed more than once

- Accounts that are closed but still showing as open

- Negative items that are older than seven years and should have been removed

- Personal information that belongs to someone else — a wrong address, a misspelled name, or a Social Security number that isn’t yours

Write down every error you find. Note the bureau it appears on, the account name, account number, and exactly what is wrong. Being specific is what makes your dispute effective.

Step 4 — Dispute Every Error in Writing

Under the Fair Credit Reporting Act — the FCRA — you have the legal right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. The credit bureau is then required to investigate within 30 days and correct or remove anything that cannot be verified.

When you write your dispute letter, include the following:

- Your full name, address, date of birth, and Social Security number

- The name and account number of the item you are disputing

- A clear, specific explanation of what is wrong

- A statement of what correction you are requesting

- Copies — never originals — of any supporting documents like bank statements, payment receipts, or settlement letters

Send your letter by certified mail with return receipt so you have proof it was received. Keep a copy of everything. If you are disputing multiple errors, list each one separately and clearly in the same letter rather than bundling them together vaguely.

Once the bureau completes their investigation, they must send you the results in writing. If the item is corrected or removed, you are entitled to a free updated copy of your report.

Step 5 — Deal With Legitimate Negative Items Strategically

Disputing errors is one thing. But what do you do about negative items that are genuinely yours — late payments, collections, charge-offs?

These take more strategy but they are far from hopeless.

For collection accounts, start by contacting the collection agency in writing and asking them to validate the debt. They are legally required to prove the debt is yours and that the amount is correct. If they cannot validate it, it must be removed. If they do validate it, consider negotiating a pay-for-delete agreement — an arrangement where you agree to pay the debt in exchange for them removing the negative entry from your credit report. Get any such agreement in writing before you pay a single dollar.

For late payments, write a goodwill letter to the original creditor. This is a polite, professional letter acknowledging the missed payment, explaining the circumstances if relevant, and respectfully requesting that they remove the negative mark as a goodwill gesture — especially if your payment history with them has otherwise been clean. Goodwill letters don’t always work, but they succeed often enough to be worth sending.

For charge-offs, the account has already been written off by the lender as a loss, which means the damage is done. Paying a charged-off account won’t remove it from your report, but it changes the status from “unpaid charge-off” to “paid charge-off” — which looks better to future lenders. Some may also negotiate a pay-for-delete on charge-offs, particularly if the debt is older.

Step 6 — Start Rebuilding Positive Credit at the Same Time

This is the step most people skip entirely, and it’s a serious mistake. Removing negative items improves your score, but adding fresh positive history accelerates your recovery dramatically. Both need to happen at the same time.

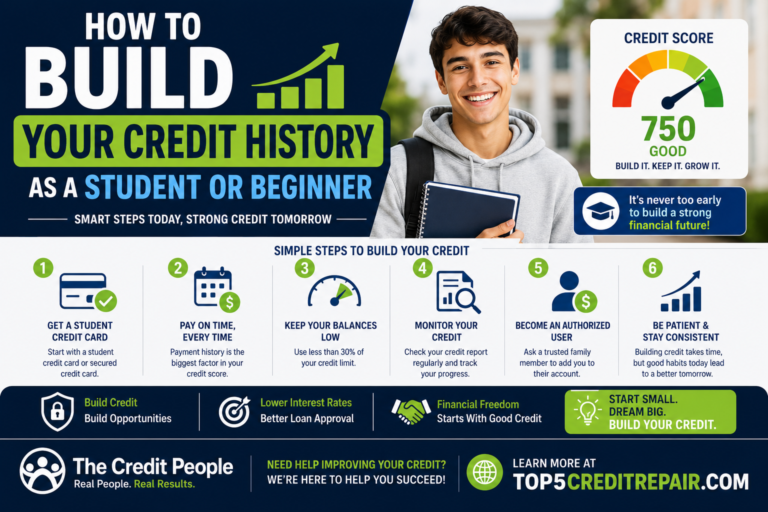

Secured credit cards are the most accessible tool for rebuilding. You deposit a small amount — usually between $200 and $500 — which becomes your credit limit. Use the card for small purchases each month, then pay the full balance before the due date. The on-time payments get reported to the bureaus and begin building positive history immediately. After six to twelve months of responsible use, many secured cards automatically upgrade to unsecured cards and return your deposit.

Credit builder loans work differently but serve the same purpose. Offered by many credit unions and online lenders, these are small loans where the money is held in a savings account while you make monthly payments. At the end of the loan term, you receive the funds and you’ve built a record of consistent on-time payments. Some of the most well-known options include Self, Credit Strong, and local credit unions that offer this product specifically to help people build credit from scratch or after damage.

Becoming an authorized user on someone else’s account is another powerful strategy — if done right. Ask a family member or close friend who has a credit card with a long history, low balance, and perfect payment record to add you as an authorized user. Their positive account history gets added to your credit file, which can give your score a meaningful boost. You don’t even need to use the card — the reporting alone is what helps. Make sure the primary cardholder is financially responsible, because if they miss a payment it will show up on your report too.

Step 7 — Build Habits That Protect Your Score Going Forward

Getting your credit repaired is only half the work. Keeping it in good shape requires a few consistent habits that become second nature over time.

Pay every bill on time, every month. Set up automatic payments for at least the minimum due on every account so you never accidentally miss a due date. Payment history is 35% of your score — nothing else comes close.

Keep your credit card balances low. Even if you pay in full every month, your balance is often reported to the bureaus before your payment posts. Try to keep your balance below 30% of your limit at all times, not just at the end of the month.

Don’t apply for multiple credit accounts at once. Every application triggers a hard inquiry. Space out any new credit applications by at least six months to minimize the impact on your score.

Check your credit report at least once a year. Errors can appear at any time and identity theft can go undetected for months. Regular monitoring means you catch problems early before they do serious damage.

Don’t close old accounts you’re not using. The age of your credit history matters. Closing an old card shortens your average account age and can lower your score even if you never use the card. Leave old accounts open unless there is a compelling reason — like an annual fee you cannot justify.

How Long Does DIY Credit Repair Actually Take?

This is probably the most common question people ask when they start this process — and deserves an honest answer.

For errors that are successfully disputed and removed, you can see score improvements within 30 to 60 days of the correction being made. This is the fastest win available in credit repair.

For high credit utilization, paying down balances produces results almost immediately — usually within one billing cycle after the new balance is reported to the bureaus.

For building new positive credit history through secured cards or credit builder loans, most people see meaningful improvement within three to six months of consistent use.

For serious negative items — bankruptcies, multiple charge-offs, foreclosures — full recovery takes longer. You are unlikely to reach a “good” credit score range in under a year if you have several major negatives, but meaningful improvement is absolutely possible within that timeframe. The seven-year clock on most negative items runs whether you take action or not, but the positive steps you take now dramatically accelerate your recovery well before those items naturally expire.

The honest bottom line: most people who follow these steps consistently and without interruption see a 50 to 100 point improvement within six to twelve months. Some see more, some see less — but steady, disciplined action always produces results.

Frequently Asked Questions About DIY Credit Repair

Can I really repair my credit myself without paying a company?

Yes, absolutely. Everything a credit repair company does — pulling reports, identifying errors, writing dispute letters, negotiating with collectors — you can do yourself for free. The law that gives credit repair companies their power is the same law that gives you those rights directly as a consumer. The main advantage of hiring a company is time and expertise, not access.

Will disputing items hurt my credit score?

No. Filing a dispute has zero impact on your credit score. The investigation process runs separately from score calculations entirely.

What is the fastest way to raise my credit score?

The two fastest moves are paying down credit card balances to lower your utilization, and disputing any errors currently dragging your score down. Both can produce results within a single billing cycle when done correctly.

Can I dispute accurate negative information just to try to get it removed?

Technically you can submit a dispute, but bureaus are allowed to label disputes as “frivolous” if there is no legitimate basis for them. More importantly, disputing accurate information without grounds is unlikely to work and wastes time you could spend on strategies that actually produce results.

Does DIY credit repair work for bankruptcies?

Bankruptcy itself — if accurately reported — cannot be disputed or removed before its scheduled expiration date (seven to ten years depending on the type). However, the individual accounts included in the bankruptcy can sometimes be addressed, and building new positive credit alongside the bankruptcy entry will still improve your overall score significantly over time.