Do It Yourself Credit Repair

If you’re dealing with a bad credit score, the most important thing is not to panic. It might feel overwhelming, but with the right steps, you can start fixing it on your own through simple credit repair efforts.

Begin by checking your credit report carefully. Look at every detail and make sure all the information is accurate and up to date. If you notice any mistakes or incorrect entries, gather any supporting documents you have and send a dispute letter to the credit bureau. Once they review your claim, they can correct errors, and those changes will be updated on your credit report. Taking it step by step like this can gradually help you rebuild your credit and improve your financial standing.

If your credit report is accurate but you’re struggling to keep up with payments, it’s better to reach out to your creditors as soon as possible. Most lenders prefer open communication and may be willing to work with you on a revised payment plan that fits your current financial situation.

Do It Yourself Credit Repair

In many cases, creditors would rather receive smaller, consistent payments than none at all. If things escalate to legal action, there’s still no guarantee they will recover the full amount owed, so many companies are open to negotiation. Being honest and proactive can help you avoid further damage to your credit and may lead to more manageable repayment terms.

If you’ve already agreed on a repayment plan with a creditor, make sure everything is documented in writing. Having a clear written agreement protects you in case any misunderstandings come up later, and it ensures both sides stick to the terms fairly.

To stay on track, build a simple monthly budget based on your income. Focus on covering essentials like bills, groceries, and transportation, and try to cut back on non-essential spending such as shopping or frequent dining out. The extra money you free up can go directly toward your debt payments.

It’s also a good idea to limit your use of credit cards while you’re rebuilding your finances. If possible, pay with cash or set strict spending limits so your balance doesn’t grow again. If you have multiple credit cards, consider keeping only a couple open—especially those with lower interest rates—and closing newer or high-interest accounts if they are not essential.

While you’re working on paying down debt, you can also build positive credit history by using a secured credit card. Since it’s backed by your own deposit, it helps you practice responsible credit use without increasing your risk. You might also explore joining a credit union, which often offers more flexible financial support than traditional banks.

With consistent payments and disciplined spending, your credit score can gradually improve. Remember, payment history plays a major role in your credit profile, so staying consistent is key. Avoiding bankruptcy and steadily managing your debt is often a better long-term solution, as it allows you to rebuild your financial future step by step with patience and commitment.

What Do It Yourself Credit Repair Actually Looks Like in Practice

Most people understand the general idea — check your report, fix errors, pay your bills on time. But when you actually sit down to do it, the process feels a lot less clear. What do you look for? Where do you start? What do you do when you find something wrong? This section walks you through the entire process from start to finish so you know exactly what to do and in what order.

Step 1 — Get Your Free Credit Reports From All Three Bureaus

The very first thing you need before you can repair anything is a full picture of where you currently stand. Your credit report is that picture. It shows every account you have open or closed, every payment you’ve made or missed, every collection account, every inquiry, and your personal identifying information.

You are legally entitled to a free copy of your credit report from each of the three major bureaus — Equifax, Experian, and TransUnion. The only federally authorized website to get all three for free is AnnualCreditReport.com. Do not pay for your reports anywhere else and do not sign up for trial subscriptions to access them. The free reports available at AnnualCreditReport.com are your legal right under federal law.

Pull all three reports at the same time. This matters because creditors do not always report to all three bureaus. An error on your Equifax report might not appear on your TransUnion report at all. If you only check one, you could miss problems that are quietly working against you on the others.

Step 2 — Know What You’re Looking For Before You Read

Before you go through your reports line by line, it helps to know what kinds of errors and problems actually appear on credit reports. Most people aren’t sure what a credit report error looks like, so they skim through without catching things that are costing them points.

Here are the most common problems to look for:

Accounts that aren’t yours. If a credit card, loan, or collection account appears on your report and you have no memory of opening it, this is either a data error — where someone else’s account got mixed into your file — or it’s identity theft. Either way, it does not belong on your report and needs to be addressed immediately.

Payments marked late when you paid on time. This is one of the most damaging errors possible. A single missed payment can drop your score by 50 to 100 points. If your records show you paid on time and the report says otherwise, that needs to be disputed right away.

Wrong personal information. Your name spelled incorrectly, an address you’ve never lived at, or a Social Security number that doesn’t match yours. These seem minor but can cause serious problems, particularly if your file has been mixed with someone else’s.

The same debt listed twice. When a debt gets sold from one collection agency to another, it sometimes gets reported twice — once by the original creditor and once by the collection agency. You should only owe this once, and having it listed twice makes your profile look far worse than it actually is.

Outdated negative items. Most negative items — late payments, collections, charge-offs — must be removed from your credit report after seven years. A Chapter 7 bankruptcy can remain for ten years. If you see anything negative that is older than its legal expiration date, it must come off.

Closed accounts showing as open. If you closed a credit card three years ago and it still appears as active and open, that misrepresents your current credit profile.

Wrong balances or credit limits. If your reported balance is higher than your actual balance, or your credit limit is listed as lower than it really is, your utilization ratio looks worse than it should — and that directly hurts your score.

Step 3 — Understand Your Credit Score So You Know What to Fix First

One of the most important things you can do before taking action is understand what actually drives your credit score up or down. Your score is calculated from five specific factors, each carrying a different weight. Once you know what they are, you can stop guessing and start focusing your energy where it matters most.

Payment History — 35%

This is the single biggest factor in your credit score. Every on-time payment you make strengthens this number. Every missed or late payment damages it. If your payment history is weak, getting every bill paid on time going forward is the most important thing you can do — full stop.

Credit Utilization — 30%

This measures how much of your available credit you are currently using across all your credit cards combined. If you have $10,000 in total credit limits and you owe $7,000, your utilization is 70% — which is very high and very damaging. The recommended threshold is below 30%. Below 10% is where you’ll see the best score results. Paying down balances is one of the fastest ways to improve your score because utilization gets recalculated every time your creditor reports your balance to the bureaus — usually once a month.

Length of Credit History — 15%

The longer your accounts have been open, the better this factor looks. This is one of the reasons you should be very careful about closing old credit cards, even ones you rarely use. When you close an old account, you shorten your average account age and lose the positive history that came with it.

Credit Mix — 10%

Having a variety of account types — credit cards, auto loans, personal loans, mortgages — shows lenders you can responsibly manage different kinds of borrowing. You don’t need to open new accounts just to improve this factor, but it’s good to understand why having only one type of credit limits your score ceiling.

New Inquiries — 10%

Every time you apply for new credit, the lender performs a hard inquiry on your report. Too many hard inquiries in a short period signals to lenders that you may be in financial trouble or taking on more debt than you can handle. Space out any new credit applications by at least six months while you’re in repair mode.

Step 4 — Write and Send Dispute Letters for Every Error You Found

Under the Fair Credit Reporting Act (FCRA), you have the legal right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. The credit bureau is then legally required to investigate your claim within 30 days and correct or delete anything they cannot verify with the original furnisher.

Your dispute letter needs to be clear, specific, and organized. Here is what every effective dispute letter must include:

- Your full legal name, current address, date of birth, and Social Security number

- The name of the account you are disputing and its account number

- A specific, clear explanation of what is wrong — not vague language like “this is incorrect” but rather “this account shows a missed payment in February 2024 however I have a bank statement confirming the payment cleared on February 3rd 2024”

- A direct statement of what correction you are requesting — removal or update

- A list of every supporting document you are attaching as evidence

- Your signature and the date

Send your letter by certified mail with return receipt requested. This gives you legal proof that the bureau received your dispute on a specific date, which matters if you ever need to escalate. Keep copies of every letter you send and every response you receive. Never send original documents — only copies.

If the bureau investigates and finds the information was accurate, they will notify you in writing. At that point you can add a 100-word consumer statement to your file explaining your side, dispute directly with the original furnisher, or file a complaint with the Consumer Financial Protection Bureau at ConsumerFinance.gov if you believe the investigation was not handled properly.

Step 5 — Handle Legitimate Negative Items With the Right Strategy

What about negative items that are genuinely yours — real missed payments, real collection accounts, real charge-offs? These cannot be disputed as errors because they are accurate. But that does not mean you are helpless.

Pay-for-delete for collection accounts. If you have a collection account, contact the collection agency in writing and propose a pay-for-delete agreement. This means you offer to pay the debt — either in full or as a negotiated settlement — in exchange for them removing the negative entry from your credit report entirely. Not every collector will agree to this, but enough do that it is always worth trying. The key rule is non-negotiable: get the agreement in writing before you send a single payment. If you pay first without written confirmation, you lose all leverage.

Goodwill letters for late payments. If you have one or two late payments on an otherwise clean account, write a goodwill letter to the original creditor. This is a professional, respectful letter where you acknowledge the late payment, briefly explain the circumstances if relevant, and politely ask them to remove it as a gesture of goodwill. Creditors who have a long positive relationship with you are more likely to honor this request. It does not always work, but it costs nothing to try and succeeds often enough to be part of every DIY credit repair plan.

Negotiated settlements for charge-offs. If a debt has been charged off, the creditor has already written it off as a loss. This does not mean the debt is gone — you still owe it, and it is still on your report. Contact the creditor and negotiate a settlement for less than the full amount if you are unable to pay in full. Some creditors will negotiate down significantly, especially on older debts. Again — written agreement before any payment.

Step 6 — Bring Your Credit Utilization Down Aggressively

If your credit card balances are high, reducing your utilization is the single fastest way to improve your credit score. Unlike building payment history — which takes months — utilization improvements show up in your score within a single billing cycle after your new lower balance gets reported.

Here is a practical approach that works even when money is tight:

Start with the card that has the highest utilization rate relative to its limit, not necessarily the highest balance. Getting one card under 30% has more impact than slightly lowering the balance on several cards. Once that card is under 30%, move to the next. If you can get every card below 10%, you will see your score improve more than almost any other single action you can take.

If paying down balances isn’t possible right now, call your credit card companies and ask for a credit limit increase. If approved, your utilization ratio drops immediately without paying anything — because the same balance now represents a smaller percentage of a higher limit. This works best if your payment history with that card has been consistent.

Step 7 — Build Fresh Positive History While You Repair the Old

Credit repair is not just about removing the bad — it is equally about adding the good. Fresh positive payment history builds month by month and over time begins to outweigh older negative marks. The two most accessible tools for doing this are secured credit cards and credit builder loans.

A secured credit card works by letting you deposit a small amount — usually $200 to $500 — which becomes your credit limit. Use it each month for a small recurring expense like a streaming subscription or grocery run. Then pay the full balance before the due date every single month without exception. The on-time payments get reported to all three bureaus and begin building positive history immediately. After six to twelve months of responsible use, many secured cards convert automatically to unsecured cards and return your deposit.

A credit builder loan is designed specifically for people rebuilding credit. You borrow a small amount, but instead of receiving the money upfront, it sits in a savings account while you make monthly payments. At the end of the loan term, you receive the money and you have a perfect payment history on your report. Credit unions, community banks, and online lenders like Self and Credit Strong offer these specifically for people in credit repair situations.

How Long Does It Take to See Real Results From DIY Credit Repair?

This is the question everyone asks and deserves a straight answer.

If you successfully dispute and remove errors from your report, you can see score improvements within 30 to 45 days of the correction being processed — sometimes faster.

If you pay down high credit card balances, the improvement shows up within one billing cycle — usually 30 days — after your lower balance is reported to the bureaus.

If you are building new positive history through a secured card or credit builder loan, expect to see meaningful movement within three to six months of consistent on-time payments.

If you are dealing with serious negative items like multiple charge-offs, bankruptcies, or foreclosures, full recovery to a good credit score takes longer — typically one to three years of disciplined effort. But your score can improve meaningfully within the first six months even with serious negatives on your report, because new positive information begins to offset older negative marks.

The honest truth is that most people who follow a structured DIY credit repair plan consistently see a 40 to 100 point improvement within the first year. Results vary depending on starting point, severity of the damage, and how consistently you follow through — but the direction is always the same when you stay the course.

Our Top Picks for Best Credit Repair Companies 2026

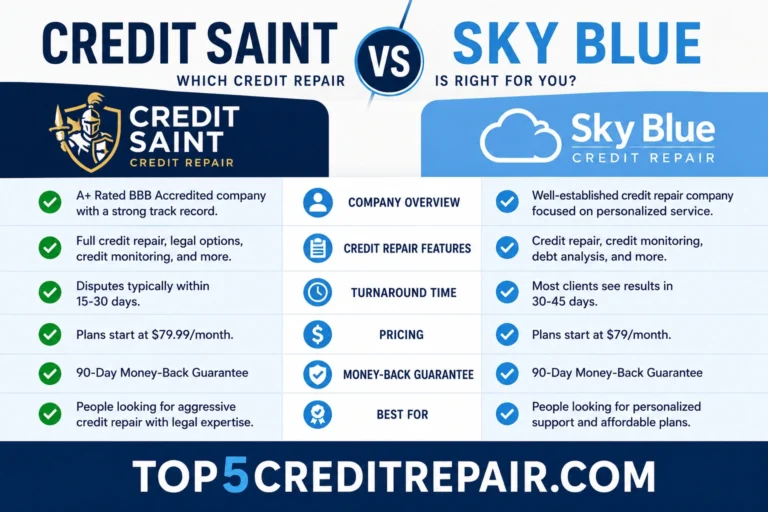

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

Frequently Asked Questions About DIY Credit Repair

Is DIY credit repair really free?

Yes. Everything involved in DIY credit repair — pulling your reports, writing dispute letters, negotiating with collectors, building credit with a secured card — can be done without paying any third party. The only cost involved is a secured card deposit, which you get back. Credit repair companies charge monthly fees for a service you can legally perform yourself.

Will disputing items on my credit report hurt my score?

No. Filing a dispute has absolutely no impact on your credit score. The investigation runs separately from score calculations entirely. Your score is not affected while a dispute is pending or after it is resolved.

Can I dispute accurate negative information?

If the information is completely accurate, a dispute is unlikely to result in removal and the bureau can label it as frivolous. However, even accurate information must be verified by the furnisher within 30 days. If the furnisher cannot or does not respond in time, the item must be removed regardless of its accuracy. This is why some legitimate negative items do get removed through the dispute process even when they are technically accurate.

What if my dispute gets rejected?

A rejected dispute is not the end of the road. You can re-dispute with stronger documentation, dispute directly with the original furnisher rather than the bureau, add a consumer statement to your file, or file a formal complaint with the Consumer Financial Protection Bureau. If you believe the bureau willfully ignored your dispute, you may also have legal recourse under the FCRA.

Should I close credit cards I’m not using?

Generally no. Closing a credit card reduces your total available credit, which increases your utilization ratio, and it can also shorten your average account age — both of which hurt your score. Unless the card has an annual fee you cannot justify or is tempting you to overspend, leaving it open and unused is almost always better for your credit.

Can DIY credit repair remove a bankruptcy?

An accurately reported bankruptcy cannot be removed before its legal expiration — seven years for Chapter 13, ten years for Chapter 7. However, errors within the bankruptcy listing — such as accounts included in the bankruptcy still showing as active or unpaid — can absolutely be disputed and corrected. Building positive credit aggressively alongside a bankruptcy on your report also dramatically improves your score over time