DIY Credit Repair vs Hiring a Company: Which One Actually Works?

Your credit score just came back at 562. You stare at the number on your screen, and your stomach drops. A mortgage you were counting on, a car loan you desperately need, or maybe just the embarrassment of getting declined for a store credit card — whatever brought you to this moment, one question is running through your head right now:

Do I fix this myself, or do I pay someone to fix it for me?

It’s a fair question. And the honest answer is: it depends on your situation. But before you hand over your credit card to a repair company or dive headfirst into a pile of dispute letters, let’s break down what each path actually looks like in real life.

What Credit Repair Actually Means

First, let’s clear something up. Credit repair — whether you do it yourself or hire someone — is not magic. Nobody can legally remove accurate, verified negative information from your credit report. Not you, not a $150/month credit repair company, not anyone.

What credit repair actually does is challenge inaccurate, outdated, or unverifiable information on your report. And there’s more of this than most people realize. According to a 2024 Consumer Reports survey, 44% of people who reviewed their credit reports found at least one error. That’s nearly half.

So the real question isn’t whether credit repair works — it does, when there are legitimate errors. The question is whether you need professional help to get those errors removed, or whether you can handle it on your own.

The DIY Route: What You’re Getting Into

Let’s be real about what doing it yourself involves.

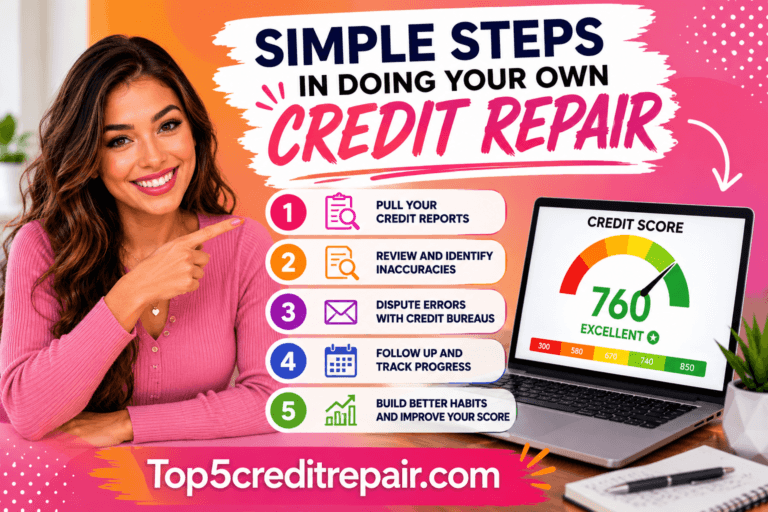

You start by pulling your credit reports from all three bureaus — Experian, Equifax, and TransUnion. You can do this for free at annualcreditreport.com. Then you go through every single line item looking for mistakes: wrong account balances, payments marked late that you paid on time, accounts that don’t even belong to you, duplicate entries, outdated debts that should have aged off.

Once you find an error, you file a dispute directly with the credit bureau online, by phone, or by mail. The bureau has 30 days to investigate. If the creditor can’t verify the item, it gets removed. If they can, it stays.

Sounds straightforward. And honestly? It kind of is — if you have the time and patience.

Click here to download Diy Credit Repair Kit

The real advantages of doing it yourself:

It’s completely free. You pay nothing to dispute errors. The process is open to every consumer under the Fair Credit Reporting Act (FCRA). The law literally gives you the right to challenge anything on your report at no cost.

You’re in full control. You see every communication. You know exactly what’s been disputed, what’s been removed, and what’s still pending. There’s no waiting on a company to send you updates.

It’s not as complicated as companies want you to think. Dispute letters don’t require legal expertise. They require your name, account number, a clear explanation of the error, and any supporting documentation you have. That’s it. The credit bureaus have online portals that walk you through the whole process.

Where DIY gets hard:

The challenge isn’t knowledge — it’s time and persistence. If you have a straightforward error on one account, DIY is a no-brainer. But if your report has a dozen negative items across all three bureaus, each requiring separate disputes, follow-up letters, and creditor negotiations, you’re looking at months of back-and-forth correspondence that can feel like a part-time job.

There’s also an emotional component. Dealing with debt collectors and creditors is stressful. Some people just don’t want to fight that battle alone. That’s a completely valid reason to consider getting help.

Hiring a Credit Repair Company: What You’re Actually Paying For

Credit repair companies do exactly what you can do yourself — they dispute errors on your behalf. The difference is that they do it professionally, at scale, and with experience navigating creditor and bureau processes.

A typical credit repair company charges somewhere between $69 and $149 per month, plus an upfront setup fee that can range from $79 to $195. For that money, you get a team that reviews your credit reports, identifies disputable items, drafts and sends dispute letters to the bureaus, and in some cases sends intervention letters directly to creditors.

Companies like Credit Saint, Sky Blue Credit, and The Credit Pros also include extras — credit score monitoring, identity theft protection, debt validation letters, and goodwill intervention letters. These are tools that go beyond basic disputes and can be genuinely useful depending on your situation.

Where hiring a company makes sense:

You have a lot of negative items. If your report is a mess — multiple collections, charge-offs, late payments across different accounts and bureaus — a professional service can tackle everything simultaneously in an organized way. What would take you a year of DIY effort might get handled in a few months.

You don’t have time. If you’re working two jobs, raising kids, or simply don’t have bandwidth to manage a multi-month dispute process, paying someone to handle it for you has real value. Time is money.

You’ve already tried and hit a wall. Sometimes creditors push back, bureaus close investigations without removing items, or you’re not sure how to escalate. Credit repair professionals know how to respond to these situations. They’ve seen every scenario.

You need guidance beyond just disputes. The better credit repair companies provide credit coaching, help you understand what’s dragging your score down, and teach you how to rebuild once the negative items are gone. That educational component can be genuinely valuable if you’re new to all of this.

Where hiring a company gets risky:

The credit repair industry, unfortunately, has a serious scam problem. The Credit Repair Organizations Act (CROA) exists specifically because so many companies have preyed on desperate people with false promises.

Watch out for companies that:

- Demand full payment upfront before doing any work

- Guarantee specific score increases (“We’ll raise your score by 150 points!”)

- Claim they can remove accurate negative information

- Tell you to dispute everything on your report, accurate or not

- Suggest creating a new credit identity

None of these things are legal. Any company making these promises is lying to you.

Legitimate credit repair companies will tell you upfront that results vary, that they can only dispute inaccurate information, and that they cannot guarantee outcomes. They’ll also give you a written contract and a three-day right to cancel.

A Honest Side-by-Side Comparison

| DIY Credit Repair | Hiring a Company | |

|---|---|---|

| Cost | Free | $69–$149/month + setup fee |

| Time required | High | Low |

| Speed of results | Depends on effort | Often faster due to experience |

| Control | Full | Partial |

| Best for | 1–3 errors, patient people | Many items, busy schedules |

| Risk | Very low | Medium (scam risk exists) |

| Legal rights used | Same | Same |

So Which Should You Choose?

Here’s the honest breakdown:

Choose DIY if:

- You have one to three clear errors on your report

- You have time to dedicate to the process

- You’re comfortable writing letters and following up

- Your budget is tight and you want to save the monthly fee

Choose a credit repair company if:

- Your report has many negative items across multiple bureaus

- You’ve already tried disputing and got nowhere

- You genuinely don’t have time to manage the process

- You want expert guidance alongside the dispute process

And if you do go with a company, stick to well-reviewed names with transparent pricing and no upfront guarantees. Read the contract. Use the three-day cancellation window if something feels off.

The Bottom Line

Here’s what nobody in this industry wants to say out loud: the tools available to a credit repair company are the exact same tools available to you. The FCRA gives every consumer the right to dispute inaccurate information for free. No company has special access, secret leverage, or a back-channel relationship with the credit bureaus.

What they do have is experience, organization, and time — and for many people, that’s worth paying for.

If your situation is simple, save your money and do it yourself. Pull your reports, find the errors, and start disputing. The process is more manageable than most people expect.

If your situation is complex, or if you’ve been spinning your wheels without results, a reputable credit repair company can absolutely help you move faster and more effectively than you might on your own.

Either way, the goal is the same: an accurate credit report that reflects who you actually are — not a collection of old mistakes that no longer tell your story.

Top5creditrepair.com Recommendation

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support