The Credit Pros vs Lexington Law (2026): Which One Is Actually Worth Your Money?

You’ve spent the last hour on Google trying to figure out which credit repair company to trust. You’ve narrowed it down to two names that keep coming up: The Credit Pros and Lexington Law. Both sound legitimate. Both have been around for years. Both promise to help you fix your credit.

But which one is actually better for your situation?

That’s exactly what we’re going to figure out in this comparison. Not a fluffy overview with vague takeaways — a real breakdown of what each company does, what it costs, where it falls short, and who should choose which one.

Let’s get into it.

The credit Pros vs Lexington Law

A Quick Look at Both Companies

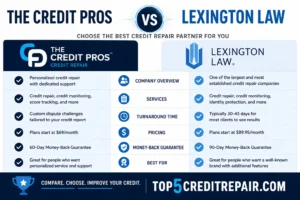

The Credit Pros launched in 2009 and has built a reputation as a tech-forward credit repair service. They’re BBB-accredited with an A+ rating and use FICO-certified professionals to help clients work through negative items on their credit reports. They also offer some features you don’t see at most competitors — like a $5,000 credit builder loan program and a mobile app for real-time tracking.

Lexington Law has been around since 2004 and is one of the most recognized names in the credit repair industry. The “law firm” branding is intentional — they actually employ attorneys and paralegals who work on your disputes. They’ve helped clients see over 83 million items removed from credit reports since opening. That’s a big number, and it’s part of why they carry so much brand weight.

Both companies are legitimate. Both follow the Credit Repair Organizations Act (CROA). And both can dispute inaccurate information on your behalf.

The differences, though, are real — and they matter depending on what you’re looking for.

Pricing Breakdown

This is where things start to diverge pretty quickly.

The Credit Pros offers three plans:

- Build Credit — $69/month: Includes a bill reminder system, debt-payoff planning tools, and TransUnion fraud alerts. Note: this plan does not include credit disputes, so it’s more of a credit-building tool than a repair service.

- Repair Credit — $129/month: This is where the actual credit repair happens. Includes unlimited disputes with all three bureaus, credit monitoring, and identity theft protection.

- Success Plus — $149/month: Everything in Repair Credit plus a $5,000 secured credit builder loan that reports to the bureaus and helps build positive payment history simultaneously.

Lexington Law has simplified things down to one plan as of 2026:

- Single Plan — $139.95/month: No upfront setup fee, but your first payment is due 5–15 days after you enroll (so essentially you’re paying within the first two weeks). Includes bureau challenges, creditor interventions, credit monitoring, identity theft insurance, and inquiry monitoring.

The bottom line on pricing: If you want full credit repair services, you’re looking at $129–$149/month with The Credit Pros vs $139.95/month with Lexington Law. They’re comparable in cost. The Credit Pros edges ahead slightly on flexibility by offering different entry points.

What Each Company Actually Does

Here’s where people get confused. Both companies dispute inaccurate items on your credit reports. But the how is different.

The Credit Pros uses FICO-certified specialists and leans heavily into technology. Their mobile app lets you track disputes, monitor your score, and manage your credit in real time. They also go beyond just disputes — their higher-tier plans actively help you build new positive credit history through the builder loan, which is something most credit repair companies don’t offer.

Lexington Law uses actual attorneys and paralegals. When your case involves complicated legal situations — like a creditor that’s ignoring dispute requests, old bankruptcies near the reporting limit, or aggressive collection activity — having a legal team behind you can make a real difference. Their Premier plan (now their standard plan) includes both bureau challenges and creditor interventions, meaning they’ll send letters directly to creditors, not just the bureaus.

Both send dispute letters. Both monitor your credit. But The Credit Pros leans on certified finance professionals and technology, while Lexington Law leans on legal expertise.

Guarantee and Refund Policy

This matters more than most people realize — because if a company doesn’t stand behind their results, that tells you something.

The Credit Pros offers a 90-day money-back guarantee. If you’re not seeing progress after three months, you can request a refund. That’s a longer and more generous window than most competitors offer.

Lexington Law offers no money-back guarantee at all. Their policy is that you can cancel anytime, but they don’t refund past payments. Given that they charge for work done during your first 5–15 days before your first payment even hits, this is worth thinking about.

If peace of mind and low risk matter to you, The Credit Pros wins this round clearly.

The Legal Trouble Question

You might have seen headlines about both of these companies. Let’s address them directly because glossing over this would be doing you a disservice.

Lexington Law faced a major lawsuit from the Consumer Financial Protection Bureau (CFPB) alleging deceptive marketing and telemarketing violations. Their parent company, PGX Holdings, filed for Chapter 11 bankruptcy in June 2023 as a result. Lexington Law itself has maintained it continues to operate and serve clients, and as of 2026 the company is still active. But the legal history is there, and it’s worth knowing.

The Credit Pros had a separate incident back in 2012 when the Idaho attorney general found them operating without a license in that state. They paid $1,000 in restitution and became fully compliant. It was a minor regulatory issue by comparison, and they’ve operated without major legal problems since.

Neither company is a scam. But if legal history is a factor in your decision, Lexington Law’s situation is more significant.

Availability

The Credit Pros is not available in Maine, Minnesota, Oregon, and Kansas.

Lexington Law is not available in Oregon.

If you’re in one of those states, your choice may already be made for you.

Real Customer Experience

Customer reviews tell a story that pricing tables can’t.

People who like Lexington Law tend to mention the professionalism of their team, the thoroughness of their dispute process, and the educational resources available. One consumer on ConsumerAffairs wrote that after going through bankruptcy, job loss, and health problems, they “thought my credit was shot beyond repair” — and Lexington Law helped them turn it around.

People who like The Credit Pros tend to highlight the mobile app, the FICO-certified specialists, and the fact that the company feels more transparent about what they’re doing and why. The credit builder loan option also gets positive mentions from people who want to repair and build credit at the same time.

Complaints for both companies follow a similar pattern — slow results, high monthly fees, and the occasional billing dispute. These are common across the credit repair industry generally, not specific red flags for either company.

Side-by-Side Comparison

| Feature | The Credit Pros | Lexington Law |

|---|---|---|

| Founded | 2009 | 2004 |

| BBB Rating | A+ | C |

| Monthly Cost | $69–$149 | $139.95 |

| Setup Fee | Varies by plan | $0 (first payment in 5–15 days) |

| Money-Back Guarantee | 90 days | None |

| Dispute Type | Unlimited, all 3 bureaus | Bureau + creditor interventions |

| Legal Team | FICO-certified specialists | Attorneys & paralegals |

| Mobile App | Yes | No |

| Credit Builder Loan | Yes ($5,000 on top plan) | No |

| Identity Theft Protection | Yes | Yes |

| Availability | 46 states | 49 states (not Oregon) |

| Legal History | Minor 2012 incident | CFPB lawsuit, parent bankruptcy |

So Which One Should You Choose?

Here’s the honest answer, because “it depends” without any guidance is useless.

- You want a 90-day money-back guarantee and lower financial risk

- You want to repair credit AND build positive history at the same time (credit builder loan)

- You like having a mobile app to track everything in real time

- You’re bothered by Lexington Law’s legal history and bankruptcy filing

Choose Lexington Law if:

- Your credit situation is complex and you want actual attorneys reviewing your file

- You have items that may require legal escalation beyond standard dispute letters

- You’re comfortable paying without a refund guarantee

- You want one of the most established names in the industry working for you

For most people in a standard credit repair situation — some collections, a few late payments, maybe an error or two — The Credit Pros is the stronger overall package in 2026. Better guarantee, similar pricing, more features at the top tier, and a cleaner legal track record.

For people with genuinely complex situations — where the legal angle matters — Lexington Law’s attorney-backed approach still has real value, despite the company’s troubled recent history.

One Last Thing Before You Sign Up

Whichever company you choose, remember this: credit repair only works on inaccurate, outdated, or unverifiable information. No company can remove accurate negative items from your credit report — not legally, anyway. If everything on your report is accurate, credit repair isn’t the answer. Credit rebuilding is.

Both The Credit Pros and Lexington Law will tell you this on a free consultation call. If a company doesn’t tell you this and instead promises to “erase” your bad credit, walk away.

Go in with realistic expectations, choose the company that fits your situation, and give the process time. Credit repair isn’t a sprint — but it does work when the errors are real.

Disclaimer: This article is for informational purposes only. Always read the full terms and conditions before signing up with any credit repair company.