Best Credit Repair Companies in Florida

If you’re struggling with a bad credit score, you’re not alone we are with you. Millions of Americans have turned to credit repair companies to help clean up their credit reports, dispute errors, and get back on track financially. The good news is that many of these companies offer free trials and money-back guarantees, so you can get started without taking a big risk.

Not sure which credit repair company to trust in Florida? We reviewed the top options so you can find a legitimate service that fits your budget and gets real results.

We’ve done the research so you don’t have to. Below, you’ll find the Best credit repair companies in Florida that have a proven track record of helping real people improve their scores and take control of their financial future. Whether you’re dealing with late payments, collections, or simply want a better shot at getting approved for a loan — there’s an option here for you.

Looking for the best credit repair companies in Florida? We compared top-rated services to help you fix errors, boost your score, and take back control of your finances.

Best Credit Repair Companies In Florida

- The Credit Pros – Best for Comprehensive Plans

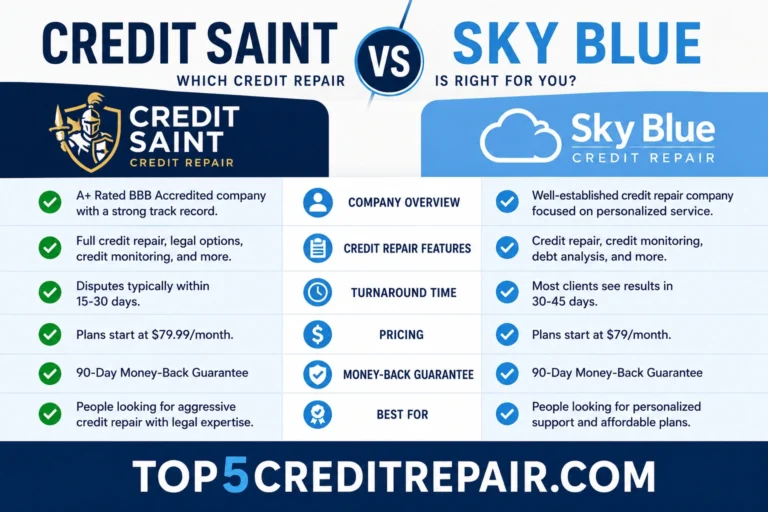

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

What Is Credit Repair?

Credit repair is the process of finding and fixing errors on your credit reports. These mistakes can sometimes hurt your credit score more than you realize. It can also play a big role in identity theft recovery — for example, removing accounts that were opened in your name without your knowledge.

When you work with a credit repair company, the process usually starts with a free consultation where they review your credit reports with you. From there, the company charges a fee to dig deeper — looking for items that are dragging your score down, accounts that don’t belong to you, and anything else that looks off.

If they find errors or items that can be challenged, the company will either file disputes directly with the credit bureaus on your behalf or walk you through how to do it yourself. Once a dispute is submitted, the credit bureaus are required to investigate and respond within a set timeframe — or remove the disputed item from your report.

How Does Credit Repair Work?

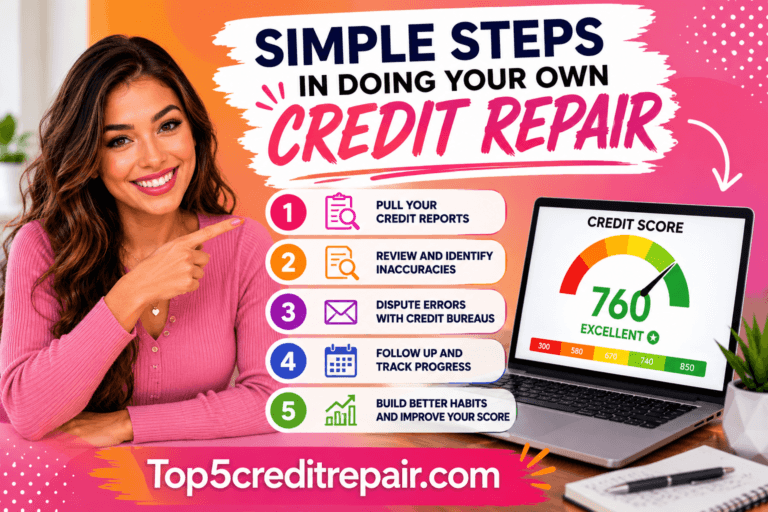

Whether you handle it yourself or bring in a professional, credit repair generally comes down to a few straightforward steps:

- Getting your credit reports from all three credit bureaus — you can pull them for free at annualcreditreport.com

- Going through each report carefully to spot anything that looks wrong or doesn’t belong

- Filing a dispute with whichever bureau is reporting the incorrect information

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute anything on your credit report that you believe is inaccurate. Once you do, the credit bureau has 30 days to look into it. If the item turns out to be wrong, they have to remove it — and they must send you the results of their investigation within five business days of wrapping it up.

One thing worth knowing: credit repair can only do so much. You — and any company you hire — can only get inaccurate information removed. If your report is error-free but your score is still low, the real fix is building better habits over time — paying bills on time, keeping your credit utilization low, and chipping away at your overall debt.

How We Chose the Best Credit Repair Companies

To put this list together, we looked at several key factors that actually matter when you’re trusting a company with your credit.

Transparency: We paid close attention to how upfront each company was about their pricing, fees, services, guarantees, terms and privacy policies. If a company made it hard to find basic information, that was a red flag for us.

Pricing and discounts: We compared plans across different price points, looking for companies that gave you real options rather than a one-size-fits-all approach. We also factored in setup fees — sometimes called first-work fees — and took note of any discounts available, like those for couples or military members.

Services: Every credit repair company will tell you they dispute inaccurate items on your report. But we leaned toward companies that went further — offering things like credit score tracking, identity theft monitoring, free consultations, creditor interventions, and letters like cease and desist or goodwill requests.

Money-back guarantee and cancellation policy: We preferred companies that stand behind their work with a refund or guarantee if they can’t get results within 90 days. We also favored those that let you walk away without hitting you with a cancellation fee.

User experience and customer satisfaction: We dug into customer reviews on third-party sites including the Better Business Bureau, and gave extra credit to companies with multiple support channels, nationwide availability, and a client portal or app to track disputes and progress.

Regulatory actions: We checked each company’s history with the FTC and searched the CFPB complaints database to see if there were any patterns of violations or unresolved customer complaints.

Warning Signs of a Credit Repair Scam

The credit repair industry has its fair share of bad actors, so knowing what to watch out for can save you a lot of trouble — and money.

According to the Consumer Financial Protection Bureau (CFPB), here are the red flags to look out for:

- They ask for payment before doing any work for you

- They promise your credit score will improve — no legitimate company can guarantee that

- They claim they can wipe your report clean, even the accurate and current negative items

- They tell you to dispute information you know is correct

- They discourage you from reaching out to the credit bureaus directly

- They never mention your rights — including the fact that you can cancel your contract within three business days of signing

- They don’t give you a written contract that spells out costs and what you’re getting

- They ask you to sign away any of your rights under the Credit Repair Organizations Act (CROA)

- They offer to set you up with a brand new credit identity or profile

- They hand out stolen Social Security numbers to clients — something that can land you in serious legal trouble, not just them

Common Credit Repair Terms to Understand

Before you start working with a credit repair company, it helps to get familiar with some of the terms you’ll likely come across:

- Creditor: A creditor is simply the institution you owe money to. They’ll work to collect what you owe, but in some cases they may be open to accepting less than the full amount — this is called debt settlement, though it can do serious damage to your credit score.

- Credit score: Your credit score is a number that reflects your credit history and tells lenders how reliable you are when it comes to repaying debt. The most widely used is the FICO score, which runs from 300 to 850.

- Credit report / credit history: Your credit report is the full record behind your score. It includes your current and past credit accounts, payment history, bankruptcies, and other financial details that lenders use to size you up.

- Unsecured debt: This is debt that isn’t tied to any physical asset. Unlike a mortgage or car loan — where the lender can take the property if you stop paying — unsecured debt leaves creditors with fewer options if you default.

- Bankruptcy: When someone simply cannot repay what they owe, bankruptcy is a legal process that can discharge that debt. In some identity theft situations, credit repair can help you avoid reaching that point. Just keep in mind that bankruptcy carries serious long-term damage to your credit.

- Debt consolidation: If you’re juggling multiple loans, debt consolidation lets you roll them into one single loan — ideally with a lower interest rate — so you’re making one monthly payment instead of several. The goal is to simplify your debt and lower what you pay each month overall.

- Financial plan: Working with a credit repair company is just one piece of the puzzle. A solid financial plan goes beyond budgeting — it helps you set clear short-term and long-term goals and gives you a roadmap for actually reaching them.