How to Remove Hard Inquiries From Your Credit Report

The honest guide to what you can actually remove, what you’re stuck with, and why most advice on this topic is half-true at best

You applied for something — a credit card, a car loan, an apartment, maybe a store card you didn’t even end up opening — and now there’s a hard inquiry sitting on your credit report. Someone told you it will drop your score. Someone else told you that you can dispute it off. A third person told you it doesn’t matter at all.

All three of those people were partially right and partially wrong, which is the exact kind of answer that makes people more confused than when they started.

So let’s go through this properly. What hard inquiries actually are, how much they actually hurt you, which ones you can legally remove, how to do it step by step, and what to do about the ones you’re genuinely stuck with. No filler, no scare tactics, no false promises.

What a Hard Inquiry Actually Is

Every time you apply for new credit — a credit card, a mortgage, an auto loan, a personal loan, a student loan — the lender pulls your credit report to evaluate whether to approve you. That pull is recorded on your credit file as a hard inquiry. It signals to future lenders that you recently sought new credit.

A hard inquiry is different from a soft inquiry, which happens when you check your own credit, when a pre-approval offer gets generated, or when an employer does a background check. Soft inquiries don’t affect your score at all and aren’t visible to lenders — only you can see them on your report. Hard inquiries are visible to lenders and do affect your score, at least temporarily.

Hard inquiries stay on your credit report for two years. However — and this is important — FICO scoring models only consider hard inquiries that occurred within the past twelve months when calculating your score. So an inquiry from 14 months ago is visible on your report but has no impact on your current score. It’s sitting there as a historical record, but it’s not hurting you anymore.

How Much Does a Hard Inquiry Actually Hurt Your Score?

Here’s where most articles either catastrophize or dismiss, and neither is accurate.

The average hard inquiry lowers a FICO score by fewer than 5 points. For most people, a single hard inquiry is barely noticeable in their score — especially if the rest of their credit profile is healthy. Someone with a 750 score who applies for one credit card might drop to 746 temporarily. That’s not a crisis.

Where inquiries become genuinely damaging is in two specific situations.

When you have multiple inquiries in a short period from different types of credit. Applying for a car loan, a personal loan, and two credit cards in the same month sends a signal that you’re aggressively seeking new credit. Each inquiry is a small hit, but five or six of them together can represent a 20–30 point drop — and more importantly, they signal desperation to lenders evaluating your application manually.

When your score is already marginal. If you’re sitting at 668 and need 680 for a loan program, a 5-point hit from an inquiry can actually matter. At 750, you have breathing room. At the borderline, you don’t.

The rate-shopping exception is real and worth knowing. If you’re shopping for a mortgage, auto loan, or student loan — and you make multiple applications within a short window — FICO scoring models recognize this as rate comparison, not credit desperation. Multiple mortgage inquiries within a 45-day window count as a single inquiry for scoring purposes. This is built into the model, so don’t avoid comparison shopping for major loans out of inquiry fear.

The Truth About Removing Hard Inquiries: What’s Legal, What’s Not

This is where a lot of online advice drifts into either dishonesty or oversimplification. Let’s be precise.

You can legally dispute and remove hard inquiries that were made without your authorization. This is the legitimate basis for hard inquiry removal. If a company pulled your credit without your knowledge or permission, that is a violation of the Fair Credit Reporting Act (FCRA). You have the legal right to dispute that inquiry and have it removed.

You cannot legitimately dispute and remove hard inquiries that you authorized. If you applied for a credit card and the issuer pulled your credit, that inquiry is accurate. Filing a dispute claiming you didn’t authorize it would be filing a false dispute — which is technically fraud, even if the credit bureaus sometimes remove items simply because the furnisher doesn’t respond in time. The fact that something might work doesn’t make it legal or ethical, and it doesn’t make it a reliable strategy.

This distinction matters because a huge amount of credit repair content online — including advice from some companies that charge for this service — conflates the two. They imply that all hard inquiries are disputable. They’re not. Only unauthorized ones are.

So the first step in any hard inquiry removal process is figuring out which category each inquiry falls into.

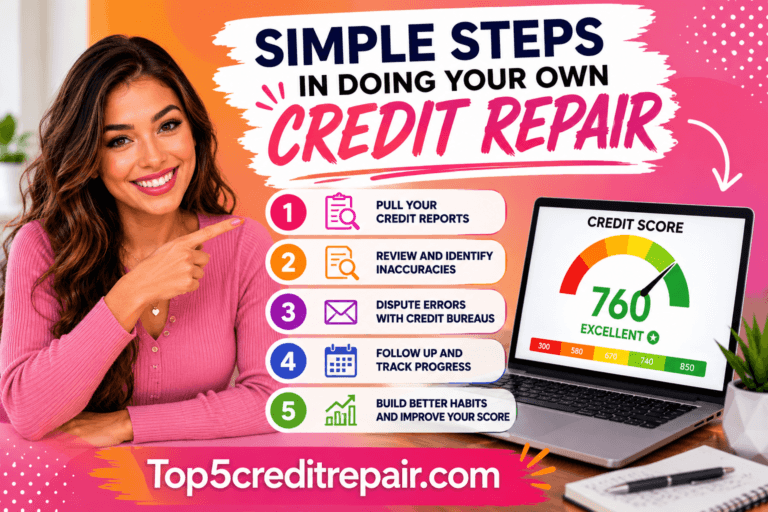

Step 1: Pull All Three of Your Credit Reports and Audit Every Inquiry

Go to AnnualCreditReport.com and pull your reports from all three bureaus — Equifax, Experian, and TransUnion. Hard inquiries are typically listed at the end of each report in a section called “Inquiries” or “Requests for Your Credit History.”

For each inquiry, note:

- The name of the company that pulled your credit

- The date of the inquiry

- Which bureau it appears on

Now go through each one and honestly ask yourself: did I apply for something with this company around that date? Think carefully. Did you apply for a store card at checkout? Did someone run your credit for an apartment? Did you fill out a financing application for furniture or electronics? Did you call your insurance company about an auto policy and they ran credit?

Companies that legitimately pull credit without you thinking of it as a “credit application” include: insurance companies in some states, landlords or property management companies, some utility companies requiring deposits, and car dealerships where you “just wanted to see your options.” These may feel unauthorized because you didn’t consciously apply for credit, but if you gave them your Social Security number and signed anything, you likely authorized the pull somewhere in the paperwork.

After your honest audit, make two lists:

List A: Inquiries I genuinely did not authorize. You have no memory of applying, you never gave this company your SSN, or the company name is completely unrecognizable and you’ve checked what it is and still don’t recognize it.

List B: Inquiries I probably authorized, even if I barely remember it.

You’re going to pursue List A. List B you’re going to leave alone or let expire naturally.

Step 2: Dispute Unauthorized Inquiries — The Right Way

For every inquiry on List A, you’re going to file disputes with the relevant credit bureaus. Here’s how to do it properly.

Write a dispute letter for each unauthorized inquiry. Don’t use the online portal for this — use certified mail with return receipt. This creates a legal paper trail that matters if the dispute escalates.

Your dispute letter should include:

- Your full name and address

- Your Social Security number (last four digits is fine for this)

- The specific inquiry you’re disputing — company name, date, and bureau

- A clear statement that you did not authorize this credit pull

- A request that the inquiry be removed under the FCRA

Keep your language factual and specific. Don’t use template language from websites that say things like “I demand immediate removal under all applicable laws.” That sounds like a form letter and gets treated like one. Write like a person explaining a genuine problem.

Send the letter to the bureau where the inquiry appears. Each bureau has its own dispute address:

- Equifax: P.O. Box 740256, Atlanta, GA 30374

- Experian: P.O. Box 4500, Allen, TX 75013

- TransUnion: P.O. Box 2000, Chester, PA 19016

Also send a letter directly to the company that pulled your credit. The bureau will contact them anyway during the investigation, but sending a direct letter establishes the dispute on both fronts and sometimes resolves things faster.

The bureau has 30 days to investigate. If the company that pulled your credit cannot verify that you authorized the inquiry, it must be removed. If the bureau doesn’t respond within 30 days, it must be removed.

Keep every piece of paper. Note the date you sent the certified letter. Keep the return receipt. If the bureau comes back saying the inquiry has been verified and will remain, you have two escalation options.

Step 3: Escalate If Necessary

Not every dispute resolves cleanly the first time. If your dispute is denied and you genuinely believe the inquiry was unauthorized, you have real escalation paths.

File a complaint with the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov/complaint. This is free, takes about ten minutes, and carries actual weight. Companies are legally required to respond to CFPB complaints, and bureaus take them seriously. Many disputes that got nowhere directly resolve quickly after a CFPB complaint is filed.

File a complaint with the Federal Trade Commission (FTC) at reportfraud.ftc.gov. The FTC doesn’t resolve individual disputes, but patterns of complaints against specific companies influence enforcement actions.

If the unauthorized inquiry appears connected to identity theft — multiple inquiries you don’t recognize from different companies around the same period — file a fraud alert with one bureau immediately (it automatically notifies the others), get an identity theft report from IdentityTheft.gov, and place a credit freeze on all three bureaus until you’ve worked through the situation. Inquiry removal is a secondary concern when identity theft is possible; stopping further damage is primary.

What About the Inquiries You Can’t Remove?

Let’s be honest about List B — the inquiries you authorized, the ones that are sitting accurately on your report.

You’re not removing those through any legitimate process. If you try to dispute an inquiry you know you authorized, you’re filing a false dispute. Bureaus sometimes remove things because the furnisher doesn’t respond in time — that’s a process failure on their end, not a legitimate removal strategy, and building your credit repair plan around gambling on process failures is not a real plan.

What you do with legitimate inquiries is: wait.

Hard inquiries stop affecting your FICO score after 12 months. They fall off your report entirely after 24 months. That timeline is fixed, it’s not that long in the scheme of your financial life, and the impact of any single inquiry is small enough that the best strategy is usually to stop worrying about it and focus on the factors that move scores significantly — payment history, utilization, account age.

If you’re applying for a mortgage or major loan in the near future and you’re concerned about inquiry count, stop applying for new credit now. Every additional inquiry compounds the signal. Freeze your application activity and let the existing inquiries age.

If a lender questions a cluster of inquiries during underwriting — which they sometimes do — you can explain them. “I was rate shopping for an auto loan” or “I was comparison shopping for credit cards before I chose one” are legitimate explanations that underwriters hear regularly. Recent rate-shopping inquiries within the FICO window of a single inquiry count are almost never a serious underwriting problem when explained.

The Credit Repair Company Question

A number of credit repair companies offer hard inquiry removal as a service. Some charge specifically for it. Here is the honest assessment of what they can and cannot do.

They can submit dispute letters on your behalf more efficiently than you might do yourself, especially if you have many inquiries to review across all three bureaus. If organization and follow-through are challenges for you, a company that handles the paperwork is a legitimate time-saver.

They cannot remove authorized hard inquiries through any legal means that you can’t access yourself for free. If a company promises to remove all your hard inquiries — including ones you clearly authorized — they are either planning to file false disputes on your behalf (which carries legal risk for you) or they’re overpromising.

The most legitimate use of a credit repair company for hard inquiry issues is as part of a broader credit review — where they’re auditing your entire report, disputing multiple types of errors including inquiries, and working on your full credit picture simultaneously. Paying a company specifically and only to dispute hard inquiries is rarely worth the cost given that the process is straightforward and free when you do it yourself.

The Bigger Picture on Hard Inquiries

Here’s the perspective worth holding onto: hard inquiries are one of the smallest factors in credit scoring. Payment history, credit utilization, length of credit history, and credit mix all carry more weight. Someone losing sleep over two hard inquiries while carrying 70% utilization on their cards is focusing on the wrong problem.

Remove the unauthorized ones — you have every right to, and the process exists for exactly that reason. Let the authorized ones expire. And redirect your energy toward the variables that actually determine whether a lender says yes or no.

The inquiry sitting on your report from last March is not what’s standing between you and the financial life you want. The habits you build from this month forward are.

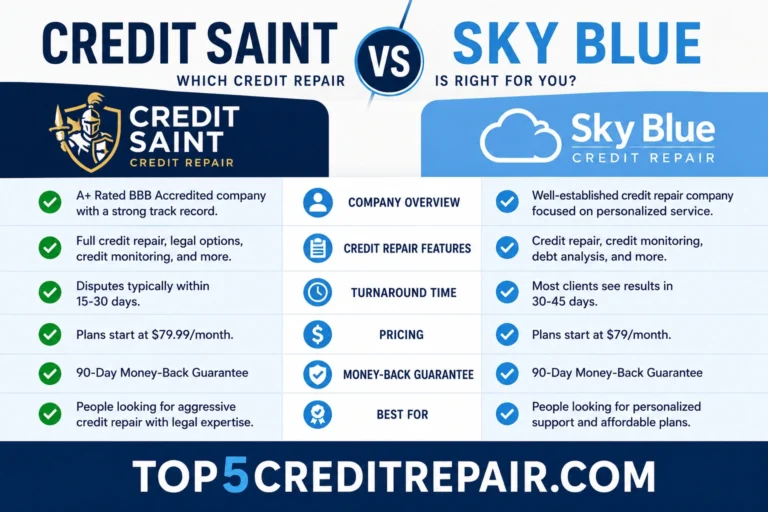

Our Recommendation Top 5 Credit Repair Companies

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

This article is for informational purposes only and does not constitute financial or legal advice. Credit reporting laws and bureau procedures can change. Verify current dispute addresses and processes at each bureau’s official website before submitting.