Can a Charge Off Be Removed From Your Credit Report?

Yes — a charge off can be removed from your credit report. It is not permanent, and you have real options to dispute, negotiate, or wait it out. If you have a charge off hurting your credit score right now, this guide will show you exactly what to do.

We help people remove negative items from their credit reports every day. A charge off is one of the most damaging marks you can have — but it is also one that can be challenged and removed with the right approach.

What Is a Charge Off?

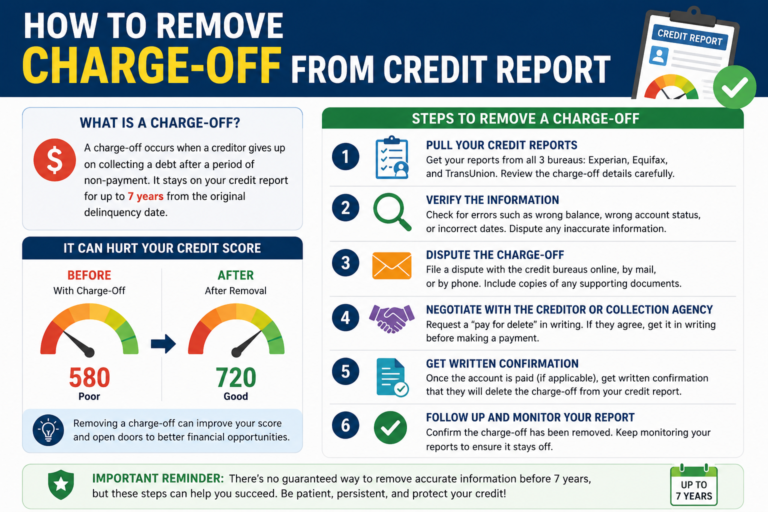

A charge off happens when a creditor gives up trying to collect a debt and writes it off as a loss on their books. This usually occurs after you have missed payments for 120 to 180 days in a row.

Here is the important thing to understand: a charge off does NOT mean the debt disappears. You still legally owe the money. What changes is that the creditor has stopped trying to collect it internally and may sell it to a debt collection agency.

A charge off appears as a negative item on your credit report and can drop your credit score by 50 to 150 points depending on your overall credit history. It stays on your report for up to 7 years from the date of the first missed payment.

How Much Does a Charge Off Hurt Your Credit Score?

| Credit Score Range Before | Estimated Drop |

| Excellent (750+) | 100 to 150 points |

| Good (700-749) | 80 to 120 points |

| Fair (650-699) | 50 to 80 points |

| Poor (below 650) | 20 to 50 points |

The higher your score before the charge off, the more damage it causes. This is because people with excellent credit have very few negative marks, so one charge off stands out significantly.

can a charge off be removed from your credit report

Yes it take time But you Can remove easily.

Can a Charge Off Be Removed Before 7 Years?

Yes. There are three proven ways to remove a charge off from your credit report before the 7-year period ends:

Method 1: Dispute the Charge Off (Free)

If the charge off contains any errors or inaccuracies, you have the right to dispute it with the credit bureaus under the Fair Credit Reporting Act (FCRA). The bureau must investigate within 30 days.

Common errors that can get a charge off removed:

- Wrong account balance listed

- Incorrect date of first delinquency

- Charge off belongs to someone else

- Account was paid but still shows as charged off

- Duplicate entry for the same account

- Creditor cannot verify the information

How to dispute a charge off:

- Pull your credit reports from all three bureaus at AnnualCreditReport.com

- Identify every error in the charge off entry

- Write a dispute letter to Equifax, Experian, and TransUnion

- Include copies of any supporting documents

- Send by certified mail so you have proof of delivery

- Wait 30 to 45 days for their investigation result

If the creditor cannot verify the information within 30 days, the bureau must delete the charge off from your report entirely.

Method 2: Pay for Delete (Negotiation)

If the charge off is accurate, you can still try to negotiate its removal. This is called a pay for delete agreement — you offer to pay the debt in exchange for the creditor or collector removing the negative entry.

Here is how to approach it:

- Contact the creditor or collection agency in writing

- Offer to pay a portion or all of the debt

- Ask them to delete the charge off from all three credit bureaus as part of the agreement

- Get their agreement IN WRITING before you pay a single dollar

- Make the payment once you have the written agreement

- Follow up to confirm the deletion within 30 to 60 days

Important: Never pay without getting the deletion agreement in writing first. Once you pay, you lose your leverage.

Not every creditor will agree to pay for delete. Large banks often refuse. Smaller debt collectors are more willing to negotiate. Our credit repair specialists know which creditors respond well to this approach and how to word the negotiation letter for the best results.

Method 3: Goodwill Deletion Letter

If you have already paid the charge off and it still shows on your report, you can write a goodwill deletion letter asking the creditor to remove it as a gesture of goodwill.

This works best when:

- You have a long history with the creditor

- The charge off was a one-time mistake

- You have otherwise kept the account in good standing

- You can show a genuine hardship caused the missed payments

Goodwill letters do not always work, but they cost nothing to try. A well-written letter that explains your situation honestly and shows the account is now paid can sometimes convince a creditor to remove the mark voluntarily.

What Happens When You Pay a Charge Off?

Paying a charge off is the right thing to do — but understand what it does and does not do for your credit.

What paying a charge off DOES:

- Stops the debt from being sold again to another collector

- Changes the status from ‘Charged Off’ to ‘Charged Off — Paid’

- Removes the risk of being sued for the debt

- Shows future lenders the debt is resolved

What paying a charge off does NOT do automatically:

- It does NOT remove the charge off from your credit report

- It does NOT immediately raise your credit score significantly

- It does NOT restart the 7-year clock (a common myth)

A paid charge off is slightly better than an unpaid one in the eyes of lenders, but it still damages your score. That is why negotiating deletion before or during payment is the smarter move.

Should You Pay an Old Charge Off?

This depends on how old the charge off is and your goals.

If the charge off is less than 3 years old: Yes, address it. It is actively hurting your score and lenders will see it clearly.

If the charge off is 4 to 6 years old: Consider negotiating a pay for delete or goodwill deletion. If you cannot get deletion, paying may still help if you are applying for a mortgage or major loan.

If the charge off is close to 7 years old: You may be better off waiting for it to fall off your report automatically. Paying an old debt can sometimes cause complications, especially with the statute of limitations.

Warning: Be careful about restarting the statute of limitations on old debts. In some states, making a partial payment on a very old debt can reset the clock and allow collectors to sue you again. Always speak with a credit professional before paying an old charge off.

How Long Does a Charge Off Stay on Your Credit Report?

A charge off stays on your credit report for 7 years from the date of first delinquency — meaning the date you first missed the payment that led to the charge off.

After 7 years, the charge off must be automatically removed from your report by law. If it is not removed, you can dispute it with the credit bureaus and demand deletion.

The impact of a charge off also lessens over time. A 6-year-old charge off hurts your score much less than a 1-year-old charge off, even if both are still on your report.

Can a Credit Repair Company Help Remove a Charge Off?

Yes. A professional credit repair service can significantly improve your chances of getting a charge off removed. Here is what we do that most people cannot easily do on their own:

- We know exactly which errors to look for that can get a charge off deleted

- We write legally precise dispute letters that credit bureaus take seriously

- We negotiate pay for delete agreements with creditors on your behalf

- We follow up aggressively and escalate disputes when bureaus are slow to respond

- We monitor all three credit reports and track every deletion

Many of our clients see results within 30 to 90 days. The credit repair process takes time, but having professionals handle your case means fewer mistakes and faster results.

If you are tired of a charge off dragging down your credit score, our team is ready to help. We offer a free consultation so you can understand exactly what is on your report and what can realistically be done about it.

Frequently Asked Questions

Does disputing a charge off hurt my credit score?

No. Filing a dispute with the credit bureaus does not hurt your credit score. If the dispute is successful and the charge off is removed, your score will improve.

Can a charged off account still sue me?

Yes. A charge off does not eliminate the debt or the creditor’s right to sue you. The statute of limitations on debt varies by state, typically between 3 and 6 years. After that period, collectors cannot sue you, but the charge off can still appear on your report.

Will removing a charge off raise my credit score?

Yes, significantly. Removing a charge off is one of the most impactful things you can do for your credit score. Depending on your other credit history, you could see a jump of 50 to 150 points after a successful removal.

Can I remove a charge off myself?

Yes, you can dispute a charge off yourself for free. However, the dispute process involves knowing what to look for, how to write effective letters, and how to follow up properly. Many people find that working with a professional credit repair service saves time and gets better results.

What if the credit bureau verifies the charge off?

If the bureau verifies the charge off as accurate, you can try a different approach: negotiate directly with the creditor, write a goodwill letter, or wait for the item to age off your report. A credit repair professional can advise you on the best next step based on your specific situation.

Take Action Today

A charge off is serious — but it is not the end of your credit story. Millions of people have had charge offs removed and gone on to qualify for mortgages, car loans, and credit cards with great rates.

The sooner you act, the sooner your score can recover.

Contact our credit repair team today for a free consultation. We will review your credit report, identify every negative item that can be challenged, and build a clear plan to improve your score as fast as possible.

Our Recommendation Top 5 Credit Repair Companies

- The Credit Pros – Best for Comprehensive Plans

- Credit Saint – Best for Customized Pricing

- Sky Blue Credit – Best Value

- The Credit People – Best for Low Setup Fees

- Credit Firm– Best for Legal Support

Updated: June 2026 | top5creditrepair.com